2017 Q4 Review & Outlook

We really don’t know what the future holds, nor do we claim to understand all the moving parts of the present, but here are some of our thoughts and some of those we respect. This is going to be quick & simple:

Outlook

Presumably, Vanguard is smarter than we are, so here are some excerpts from their recent economic review and market:

■ "For 2018 and beyond, our investment outlook is one of higher risks and lower returns. Elevated valuations, low volatility, and secularly low bond yields are unlikely to be allies for robust financial market returns over the next five years. Downside risks are more elevated in the equity market than in the bond market, even with higher-than-expected inflation."

■ "In our view, the solution to this challenge is not shiny new objects or aggressive tactical shifts. Rather, our market outlook underscores the need for investors to remain disciplined and globally diversified, armed with realistic return expectations and low-cost strategies."

Source: for above and graphs that follow until otherwise labeled. Vanguard economic and market outlook for 2018: Rising risks to the status quo

The Fed’s ‘normalization’ weighs large. One might wonder why, if QE were such a good deal, is getting back to ‘normal’ a big deal? They put it very delicately, indeed:

“Overall, the chance of unexpected shocks to the economy as global monetary policy becomes more restrictive is high, particularly when considering that it involves unprecedented balance-sheet shrinkage.” Source: ibid

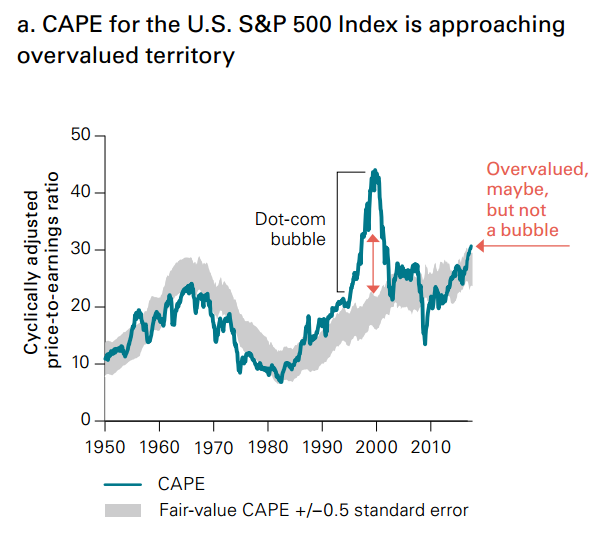

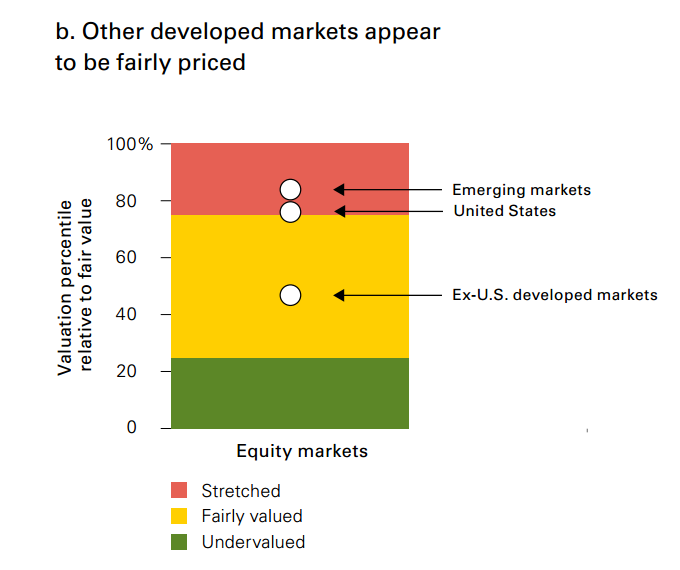

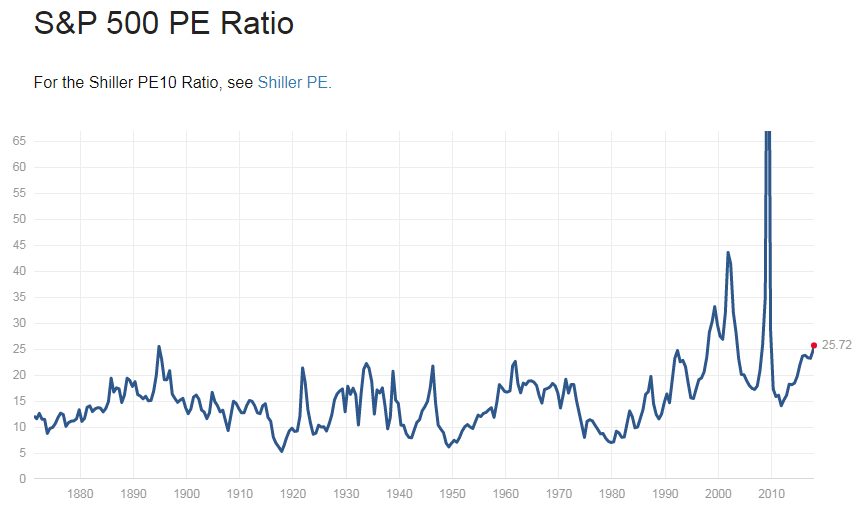

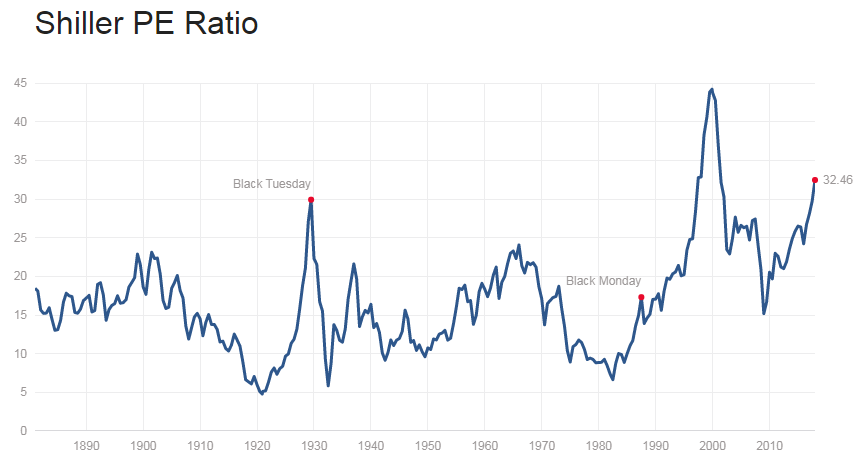

Equity valuation is always important, and we’re getting pretty lofty. From Vanguard again:

Note that Vanguard has its own proprietary version of CAPE.

We have not provided the extensive and important footnotes that accompanied these graphs. If you want to see them click here, but the analytic detail is not going to change the message on the billboard. High entry prices (ie current market valuations), higher inflation, and modest growth means lower returns. Here is the [g]estimate of returns going forward: you better sit down.

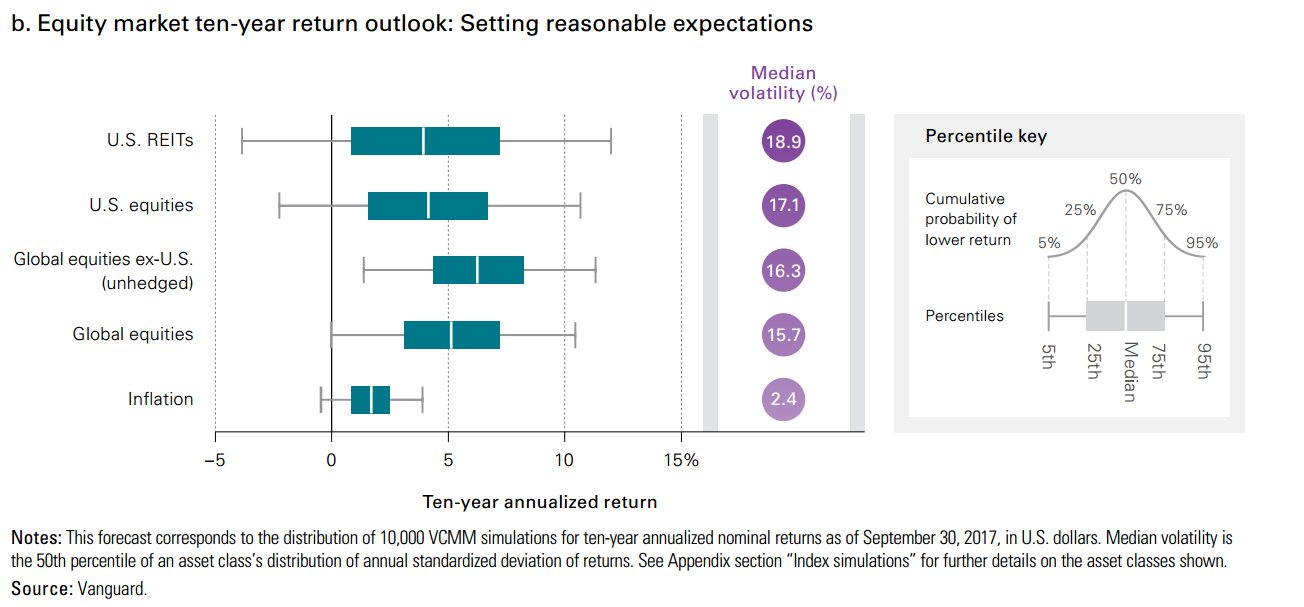

“our expected return outlook for U.S. equities over the next decade is centered in the 3%–5% range, in stark contrast to the 10% annualized return generated over the last 30 years...

“the expected return outlook for non-U.S. equity markets is in the 5.5%–7.5% range”

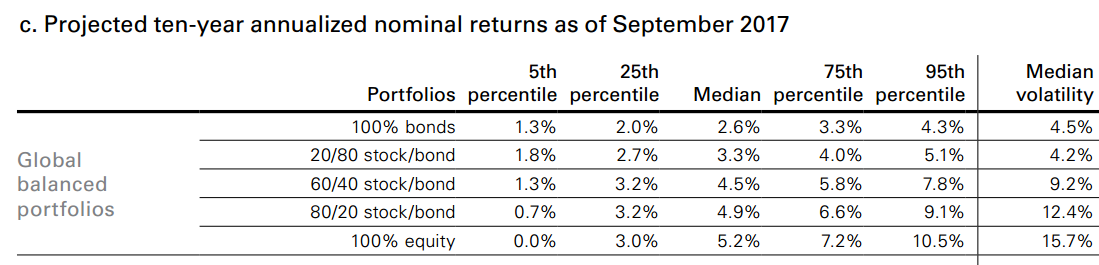

We broadly share Vanguard’s view on the markets but always remember, actual results may vary. Of course, all of these views are expressed as cloud models, as probability distributions varying over time, and while we wouldn’t dare go out ten years, we’re glad someone did... So take a look below and guess which portfolio has the highest expected Median return/Median volatility? The Engaged Reader now reaches for his calculator.

There are other issues which concern us:

-

the debt crisis (by which we mean funded debt and unfunded pension and other liabilities of corporations and governments alike)

-

adverse effects of an extended period of lower capital return on the US culture and political economy. We're thinking in context of a failed educational system which has produced innumerate students who are also illiterate in terms of American civics, economics, and history generally.

-

a seemingly structural short US$ position globally (Europe, Asia, and emerging markets). Will the Fed inadvertently set off a short US$ squeeze?

-

probability of armed geopolitical conflict in Asia or western Europe

-

it seems to us liquidity in the equity markets is qualitatively different now, presenting in microseconds and smaller lots. In fixed income it is narrow and limited, and both supported with far less financial and human capital. With modest stress liquidity may not necessarily be a continuous function.

For clarity, the words “debt crisis” convey the right meaning but an incorrect immediacy to the timeframe. The first indicia of a tsunami are often small, gentle waves. It is not an immediate crisis, but you’d best get to high ground. Today our “debt crisis” is visible only in record levels of funded federal, state and municipal debt. It has been hidden by fraudulent disclosure and dismissed or ignored by politicians as not problematic.

Unseen are the unfunded liabilities of federal, state, municipal entities. The numbers are non-trivial: some estimates are north of ~$200 trillion just for the aggregate obligations of unfunded obligations. The promises implicit in those obligations are unsustainable, and they will be broken. We’ve written about the issue in various commentary for some time, but we’re entering a new phase. The process will begin to test our economic & social fabric at a time when confidence in the equity if not legitimacy of our leaders, institutions and systems of government are in question. The timing could not be worse. Watch Connecticut, Illinois, and New Jersey. They are the canaries in the coal mine. Most crises tend to end with a bang. This one will start, not end, as the unaffordable and fraudulent generational wealth transfers engineered by corrupt politicians simply fail.

It’s all leveraged now.

What happens when pensions that value their liabilities at 8% are suddenly forced by either regulators, sober actuaries or fear of liability (civil or criminal) to mark the books to that median 4.5% return for a 60%/40% equity/fixed income portfolio that pops out of the Vanguard models? It’s starting to happen, and you get a very rude mark to market of big things like Social Security, state & municipal and a few corporate pensions. It will be a long process, and some will include massive defaults on social contracts.

Naturally, Alfred E Newman would and has synchonized this with something unhelpful and unknown: the Fed’s unwind of QE. The Fed is starting to sell off its balance sheet into fixed income markets that are disjointed and, we would argue, operating with reduced capital and impaired liquidity. Will the accrued losses on the Fed’s unwind of it’s portfolio exceed its capital? No matter, it’s the Fed!

Now this scenario would certainly resolve the mysterious disappearance of volatility which then comes back with a vengeance. Bank liquidity starts to cramp up and head for the hills, and bank capital gets a little skinny... well, we’ve seen that tape before. We stipulate that this dystopian vision is over the top, but if you slow it down to a grinding of the economic, political & social gears ... you get a sober taste of our downside scenario for the next few years. It’s not pretty for anyone. But don’t jump off that window ledge, at least yet... that’s not our expected outcome.

Geopolitical conflict

It is impossible to incorporate armed conflict into portfolio strategy until after the fact, when it is too late. Black Swan events are by definition unknown and unpredictable. Neither will prohibit us from worrying about such things or perhaps misusing the word. We are very concerned about a high probability of near term armed conflict with North Korea. It would be catastrophic, particularly for the loser, and would set off an uncontrollable cascade of knock on risks, by which we mean second order conflicts whereby other hostile entities, either independently or collectively, quickly engage to capitalize on a weakened or distracted opponent(s).

For the record and his notice we strongly criticize President Trump’s undisciplined language and mode of communication regarding North Korea.

So what to do? What not to do?

Remember, actual results may vary. No one has a clue or should be confident (aka “high conviction” in newspeak) as to any short to intermediate term outcome. Expected risk seems to be on it’s way up, expected returns seem to be on their way down for an intermediate to long term.

Recall the good old days when on the highway you saw the signs, “Next gas station 100 miles.” The prudent man checked his gas much as today’s investor should check his asset allocation and liquidity. We say that a lot because it is true a lot. It could be a bumpy ride.

We think now is not the time to embed tilts into the portfolio by concentration of asset class nor is it the time to take on or increase individual security risk. Now is the time to fully diversify if you have not. Now is not the time to run to cash and take on the full brunt of inflation risk although it is the time to make sure you have adequate liquidity... but face it, that’s just an affirmation of a continuous prudent requirement.

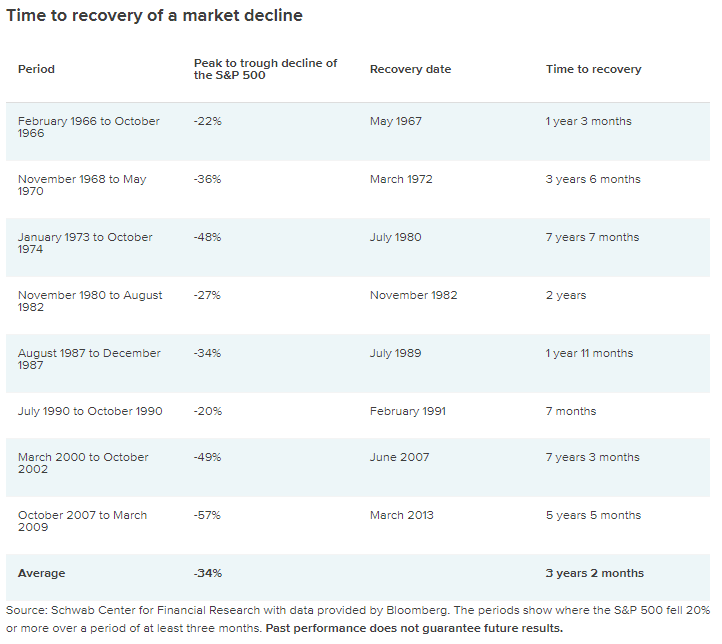

In the context of ‘check your gas’ here is some historical data on declines and recoveries of the S&P 500. We’ve found this very helpful as it clarifies risk of loss, but also timeframe of recovery... so make sure you have the liquidity to get there.

This is just static data, and Schwab appropriately points out “that the table above shows the "time to recovery" of the S&P 500 index... The time to recovery for assets held in a diversified portfolio would likely have been shorter—not considering withdrawals, if any, from the portfolio.” Our purpose in providing this information is not to scare the dickens out of investors, but to provide information that is essential to successfully managing risk.

All of this brings to mind a comment this morning of a senior executive of a global 500 corporation, not a client, who is approaching his retirement in the next year or so:

“You know, it’s not about capital accumulation anymore... it’s about capital preservation.”

Absolutely true for him. For younger people starting out the mission is entirely about capital accumulation which requires a long term timeframe, consistent periodic savings, disciplined investment into a sensible efficiently diversified asset allocation, and strict attention to efficiency of risk, cost & tax. Young people need to start now and stick to it and ride the power of compound interest. It’s all about long term beta returns and maintaining adequate liquidity.

...

A look at some data

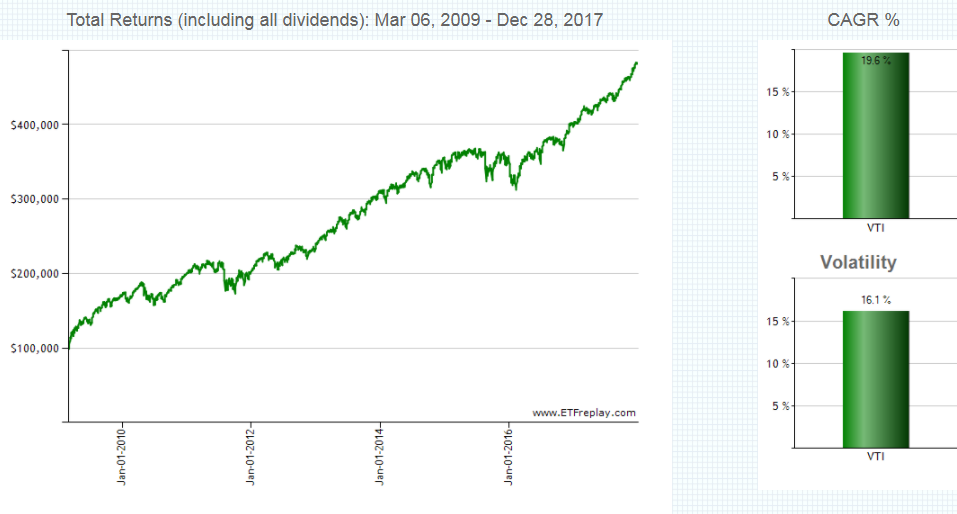

How long will the bull market last? Total returns Vanguard Total US Stock Market (VTI) since March 2009 are about 380% or just short of 20% on an annual compound basis. That's simply not sustainable.

Now look at that chart and see what happens to the value of stocks of corporations which have run sustained stock buybacks over that period and have purchased so much of their stock at, say, $100-200/share and now see it pushing $500/share? They have financed those purchases with 0% to negative real interest rates in a sea of liquidity courtesy of the Fed in what has been the largest leveraged trade in the history of markets.

If you’ve been holding equities, you may take the rest of the day off. If not, well, you’ve been on the losing side of a leveraged, large scale wealth transfer arbitrarily implemented without formal explicit legislative approval... or in fact knowledge (think of the AIG bailout specifically). Dare we say extra legal or something like that? It’s corrosive to rule of law and social stability.

Valuations: How high is up? High but OK? Or just nuts?

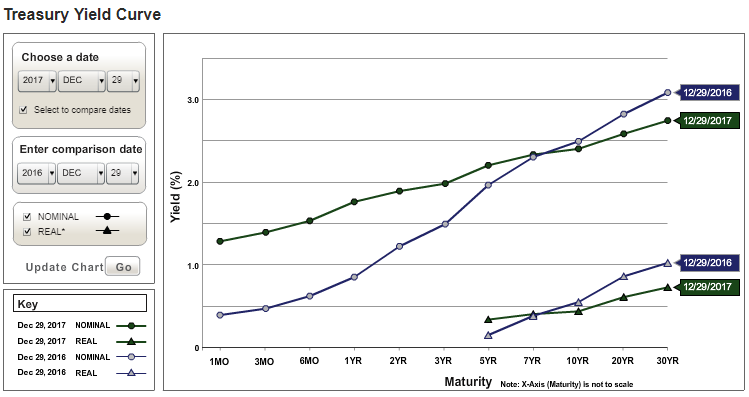

Treasury yield curve: Real intermediate & long rates dropping?

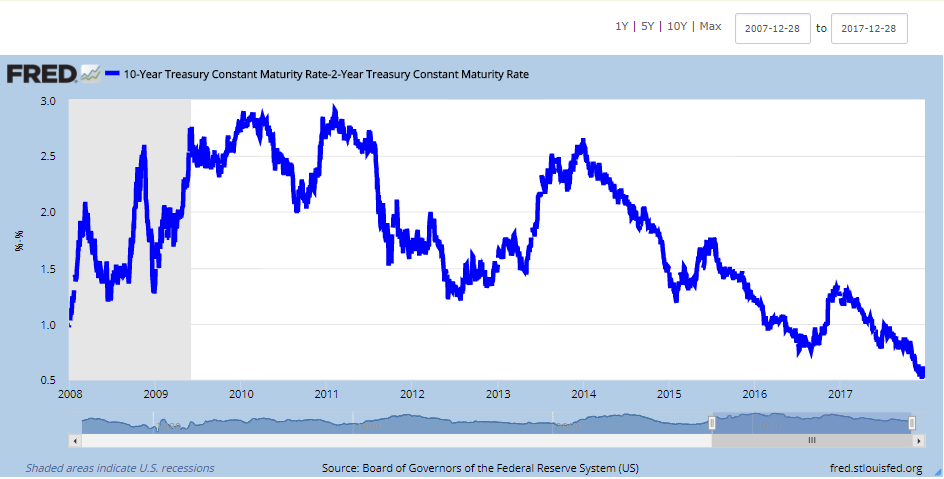

More yield curve: spread of 2 vs 10 year rates lowest in 10 years

The bond markets aren’t buying the story of continued economic strength. This is a big deal and perhaps highly problematic for the Fed’s unwind.

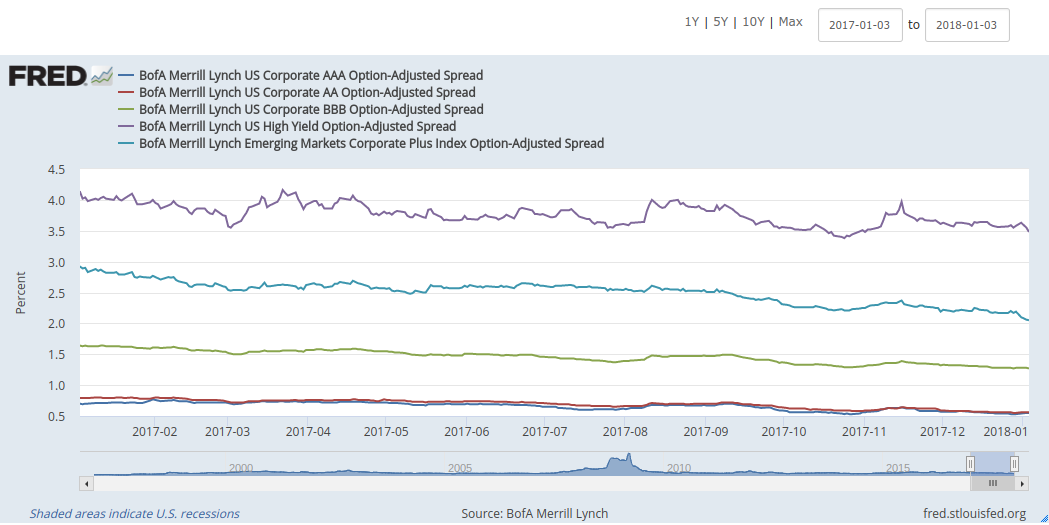

Credit spreads: compressed but stable

Oil prices have rallied significantly

If markets express views on the economy we have a huge disagreement between the oil markets and the flattening yield curve. We simply do not know how to reconcile these two important markets but note it might be symptomatic of that US$ short squeeze getting warmed up. Oil is priced in US$.

Inflation

5 year, 5 year forwards seem stable, slightly over 2%. This data reflects the expected inflation (on average) over the five-year period that begins five years from today.

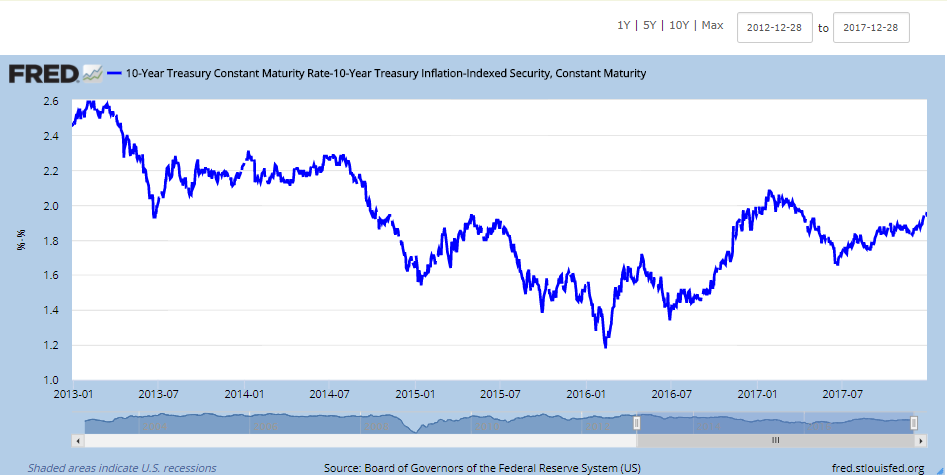

10 year nominal less 10 TIPS, slightly under 2%

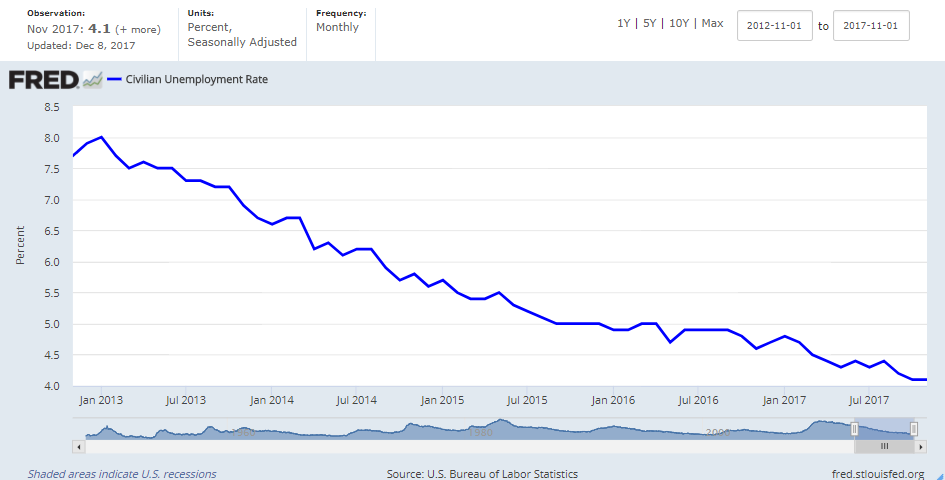

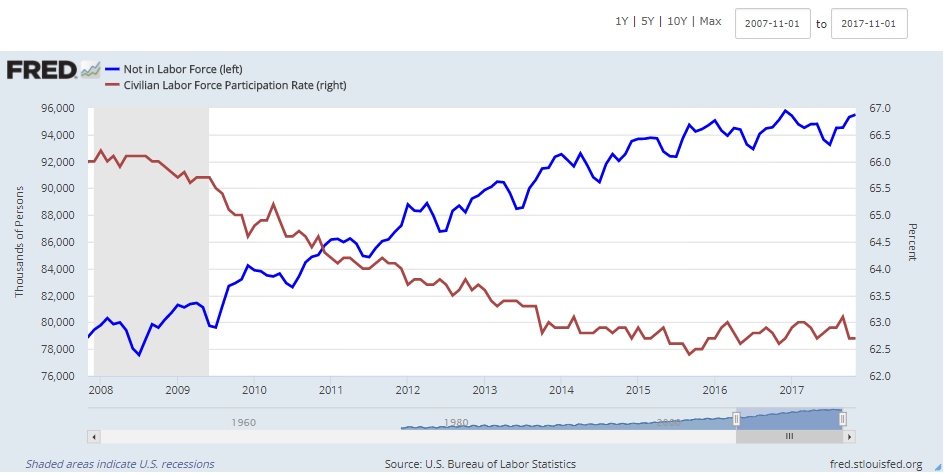

Labor markets: we still don’t vest the official ‘unemployment rate’ with much credibility.

The traditional view of the old style, official ‘unemployment’ rate presumes a certain utility to the unemployed that is available, at least in concept, to be deployed into the economy with productive result. Given the failure of the educational system and other social changes over the past two generations, one wonders if that macro assumption has lost validity. Has a portion of our working age population become impaired such as to be viewed as a liability instead of an underutilized or contingent asset?

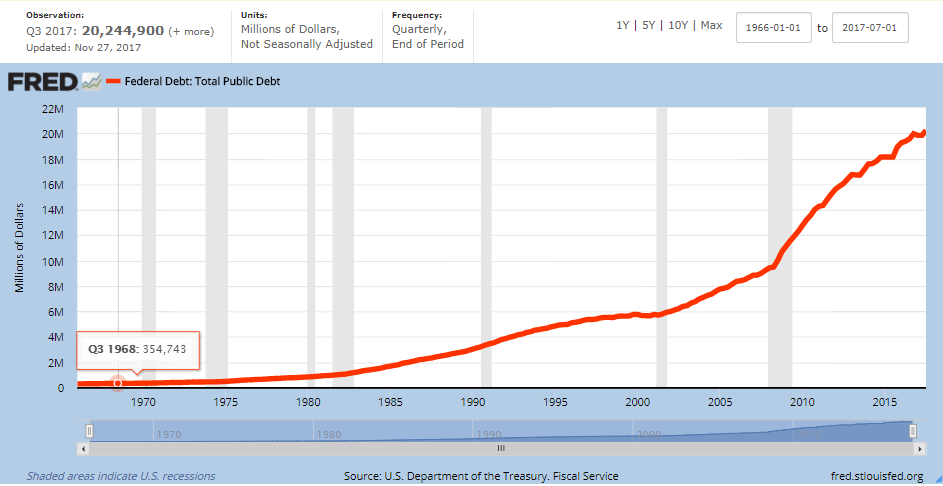

Federal debt: we all need to recognize that our federal debt, while too damn high, is a rounding error relative to our unfunded liabilities

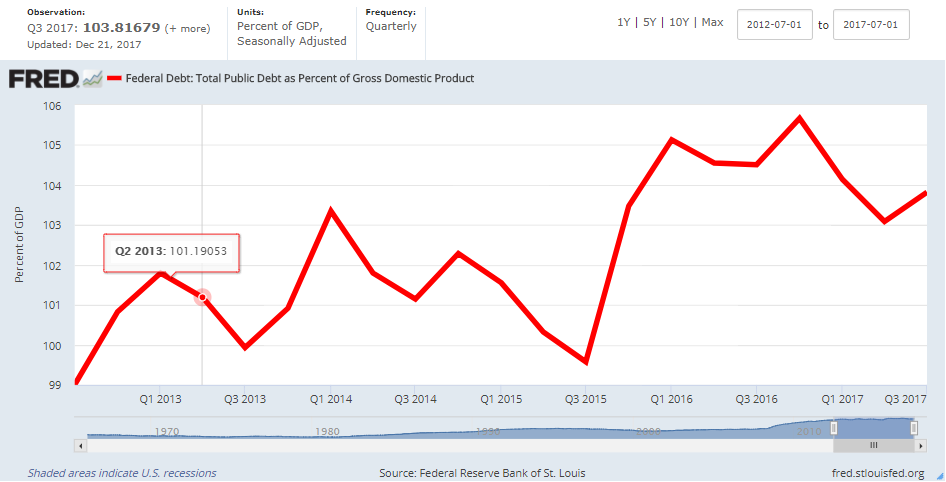

Federal debt as % GDP: 104%

GDP outlook: the Atlanta Fed is quite optimistic

We are not overly concerned about a near term recession unless the Fed creates one or the credit markets do by widening spreads. We think the recently passed tax package, while not the essence of perfection, is a significant improvement on the margin and the economy operates on the margin. We also believe the changes to US energy policy, both those enacted and proposed, are materially beneficial to the US and global economies in the intermediate to long terms.

We do not know how long the economic or market cycles will run. Hopefully, our political landscape can muster some focus to address the longer term debt crisis as we have described it. It’s not that tough: it’s simply about responsible governance. We can no longer afford frivolous expense or waste of time.

The next gas station is 100 miles, so check the gas. It might be close.

...

The very fine print. We recommend you read Vanguard’s excellent piece in whole [Vanguard economic and market outlook for 2018: Rising risks to the status quo]. Do not rely upon it or our translation, excerptation, or interpretation of it. We sure hope our use of these excerpts falls within fair use doctrine. We own a bunch of their product. We also attach to this posting, and to every reference in it, each and every exculpatory disclaimer ever known to every Wall Street law firm including actual results may vary, analysis may be wrong, we’re lying dogs, etc. While we believe the sources to be accurate, we have not independently verified the data or analysis cited here and don’t intent do. No kidding on all this stuff.

hb

hb

Reader Comments