Where's my state? Or a helpful retirement guide...

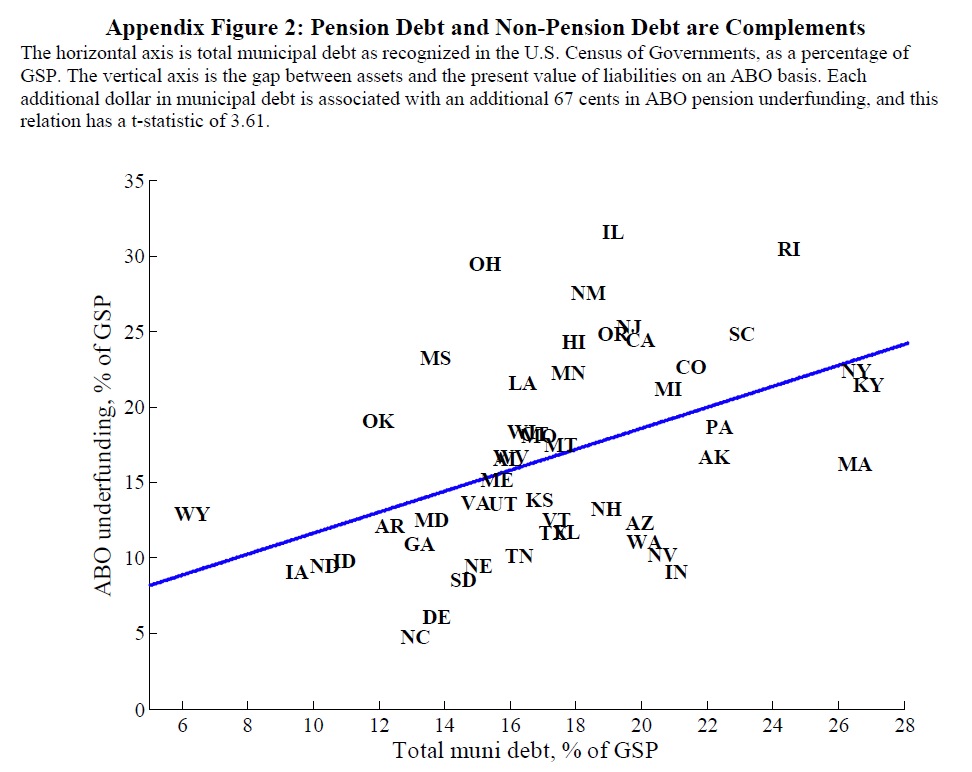

We thought we'd share this graph from The Revenue Demands of Public Employee Pension Promises of June 2011 by Robert Novy-Marx, University of Rochester, and Joshua D. Rauh, Kellogg School of Management.

This work is timely and a hugely beneficial public service, so share it with your friends. Everyone seems to be fascinated by the picture that shows by state unfunded pension liabilities plotted against municipal debt, both as a % of Gross State Product which we present below:

Anecdotally, we report a general preference by viewers, quelle surprise, for the lower left quadrant. Our sample is biased, if not entirely limited, to tax payers, and we haven't gotten to any state representatives or members of Congress ... yet.

We also note the co-ordinates of the center mass as estimated by blink test seems to be around [17%,17%]. So if we restate the financials to include All Actual Adjusted for Undervalued & Inaccurately Disclosed liabilites (AAAUID) we get the center mass at effectively 34% AAUID liabilities to Gross State Product. As a proxy that puts them in good company with Nepal, Bolivia, Democratic Republic of Congo and New Zealand as you can see here (we stipulate imperfect method, but it's close enough for government work, eh?).

We ask: why are the material liabilities of states and municipalities in need of ABO adjustments? The authors state

Plan actuaries typically assume that the expected return on their portfolios will be about 8 percent, and then measure the adequacy of assets to meet liabilities based on that expected return. This accounting standard sets up a false equivalence between relatively certain pension payments and the much less certain outcome of a risky investment portfolio..

We might suggest that an expected return of 8% might be a tad aggressive when the 10 year Treasury is yielding 2.91%? Are we to infer they are all in on equites and leveraged 'alternative assets"? There is clearly a material failure of accurate disclosure and financial reporting here. Where is the Government Accounting Standards Board (GASB)? Where is the SEC? This is how we made the mortgage and financial crisis, and no surprise it's moved to the muni sector.

Wish list: what we'd really like to see is the graph with a few more dimensions, at minimum a surface, adding total state tax burden... and perhaps regulatory cost of compliance.

All in all, great work by these guys.

hb

hb

Question: May I ask for a specific clarification on Appendix Figure 2: Pension Debt and Non-Pension Debt are Complements (as below)? How is the ABO calculated in this chart? Is the method the same as earlier described in the paper … “we use real Treasury yields (based on TIPS) to discount deflated cash flows, rather than nominal Treasury yields to discount nominal cash flows…” ?

Answer: yes. So in plain English, take the nominal pension liabilities (what the actuaries give you), then deflate them to convert to the nominal liabilities to real liabilities, then discount the real liabilities at the real Treasury rate.