2016 Q2 review & comment: nothing happened?

Our outlook is not one we encourage anyone to bet on. We see continuing weakness in the US economy, and it strikes us that the economic damage or benefit to markets from the EU will largely be a function of political decisions yet to be made.

Brexit is a signal event in the battle between democracy & the wisdom of the crowds against the great Leviathan of the regulatory state and its central planners. Think of the aggregate of markets, the collective & instantaneous grouping and expression of all known information and all preferences. This we call “price”, and on which all free persons, everyone, vote every day. In the opposing camp are the endlessly elegant and constantly revised computations of the central planners, the ‘Let X= my summer vacation” types in Brussels and Washington whose pronouncements always seem to translate to some variation of less individual freedom, less choice, and no accountability.

“We have been tempted to believe that society has become too complex to be managed by self-rule, that government by an elite group is superior to government for, by, and of the people. But if no one among us is capable of governing himself, then who among us has the capacity to govern someone else?” - Ronald Reagan

For the UK we understand that of the entire body of law and regulation effecting the lives of our British brethren, some 60% is promulgated by EU officials who are neither seated nor removed by election. This may explain how they forgot that consent of the governed is a necessary condition that needs to be maintained by any representative or republican democracy. One may recall the magnitude of change forced upon the American people by ObamaCare and carried by a single vote, bought & paid for by pork.

As to the Brexit crisis if we look at the markets as of yesterday’s close... well, nothing of any magnitude really happened. Yes, a bit of volatility, some repricing of things European, but it seemed rather mild after a bit. One can’t help but notice, or rather suspect, the aroma of the central bank plunge protection teams at work because something of magnitude did happen.

Nevertheless, the UK exit is significant… wait until Catalonia votes to leave Spain. There are a handful of these events around the corner. It is quite possible that Escape from the EU has just begun. And there is already market stress: major real estate funds have had to suspend redemptions. No bid is no exit. We might expect some further variations of this theme.

Three big asset management firms have halted trading in real estate investment funds in the last 24 hours, the latest sign of turmoil since the U.K. voted to leave the European Union on June 23.

The funds are heavily exposed to offices and other prime commercial property that can't be unloaded quickly enough when nervous investors want their money back.

Standard Life halted trading in its fund on Monday because of "exceptional market circumstances." Aviva Investors followed Tuesday, suspending its fund due to a "lack of immediate liquidity." M&G Investments said it suspended trading in M&G Property Portfolio because "investor redemptions have risen markedly" since the Brexit vote.

source: Investors bail out of U.K. real estate on Brexit shock 7/5

The real question for Brexit and the euro markets may be of duration rather than short term intensity. It is not the exit that determines the outcomes for markets, but rather how the EU reacts to it. A protectionist, regressive stance on the part of the EU would be a destructive response and could unleash longer term, powerful damaging forces. The converse holds as well, but one senses the capacity of the European Central Bank is slowly coming into question as is the feasibility of some of the peripheral and perhaps one of the major European banks.

And then, of course, we have the US election.... there are many marbles on the table.

US fixed income

Meanwhile domestically we are left with the perpetual softness of a low growth economy hampered by the continuing policy issues we previously and excessively discussed: the framework and causation of slow growth is unchanged. The problems compound.

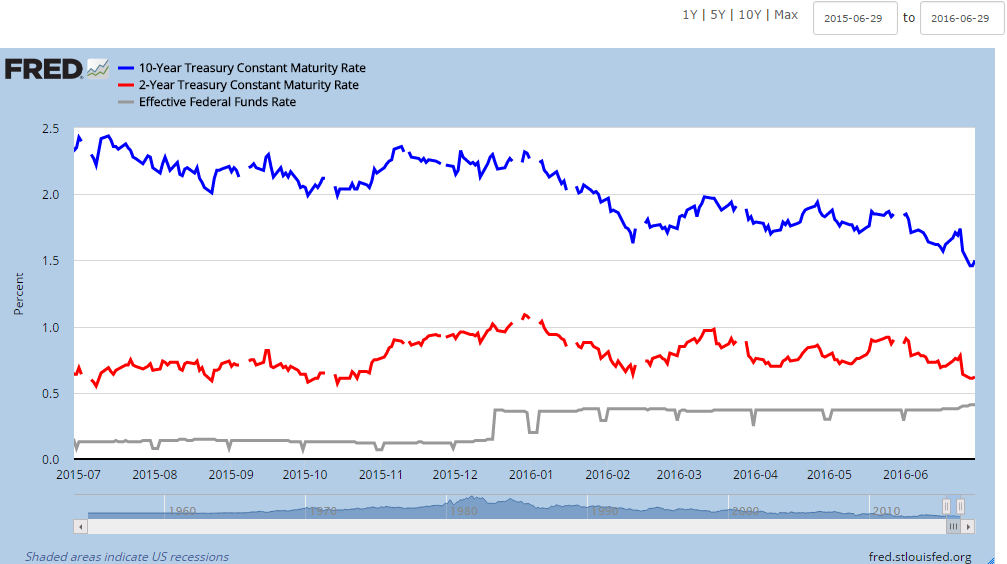

Interest Rates

Below we see rates of 10 & 2 year Treasuries and the effective funds rate. Recall the Fed talking about raising rates in a ‘full employment’ economy? See the decline of 2’s and 10’s? The Fed has spent it’s last credibility. There is no sign of upward pressure, even pre Brexit. Do we have decreasing demand for money? Perhaps but it is also hard to underestimate the flight money coming into the US$. Both?

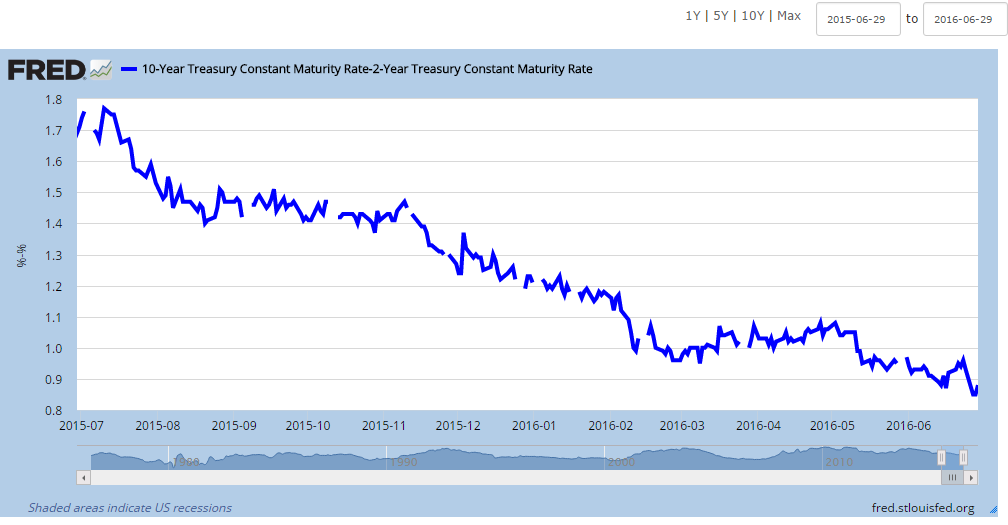

More troubling is the continuing decline 10 - 2’s spread. Strengthening economies tend to generate yield curves that steepen rather than flatten. Negative yield curves tend to be fairly good leading indicators of recessions.

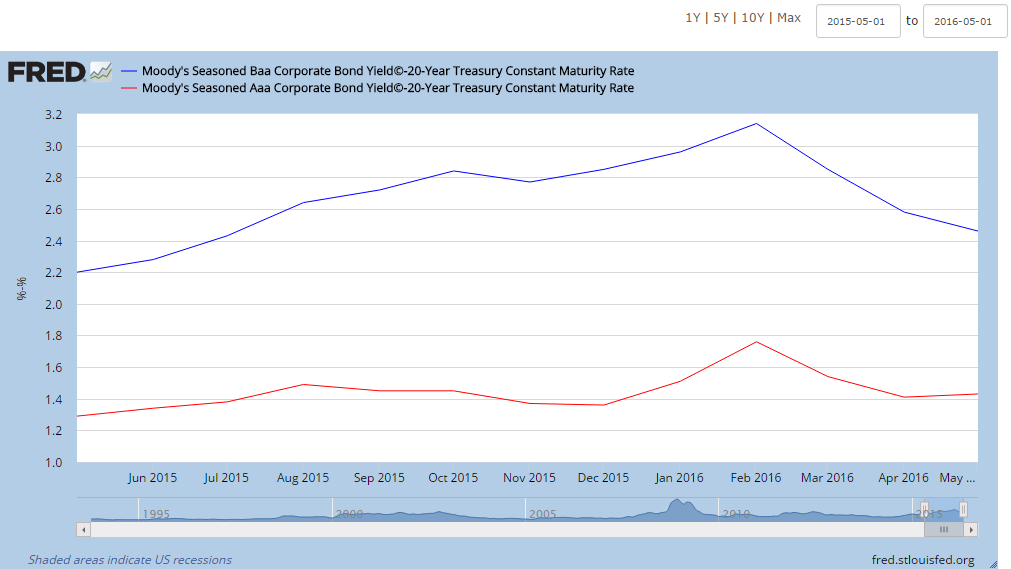

Credit spreads

Corporate spreads seem to have benefitted from the flight to quality of Brexit and the negative rates of many sovereign issuers in Asia and Europe. Some yield is better than negative yield, and US investment grade credits are arguably superior credits to many sovereigns, although opinions would vary on that, particularly those of certain European finance ministers. The decline of these spreads is good for investors that own them, perhaps less so for new buyers who get lower spreads. Is this an indirect indication of eroding credit quality of sovereign debt?

High yield spreads have also declined, driven mostly we suspect by the modest recovery in oil prices and the search for yield. Rising energy prices, even modestly so, will tend to increase both cash flow and recovery values in distressed energy assets.

In the meantime where does money seeking a safe haven go? Well, notwithstanding Mrs. Clinton’s vaunted Reset with Russia, not to Mr.Putin’s Russian Ruble, nor to the €uro which just blew up, and certainly not to Chinese Yuan. China has its own acute problems with capital flight. The safe haven money comes to US Treasuries, investment grade US debt, and US equities and in that order.

The bid for US fixed income, driven by higher rates and better credit quality, will strengthen. One suspects we will see the 10 year Treasury march lower over the course of this year regardless of what the Fed says or does. This in turn will pressure domestic fixed income investors, both institutions and retail investors, and threaten the viability of meeting longer term return objectives of fixed income portfolios.

Our “data dependent” Fed seemingly has discovered that new data comes out everyday, and this provides a viable framework for continuous introspection. It’s a new dawn every day for Team Janet. They have lost whatever control they thought they had.

Some things that bother us:

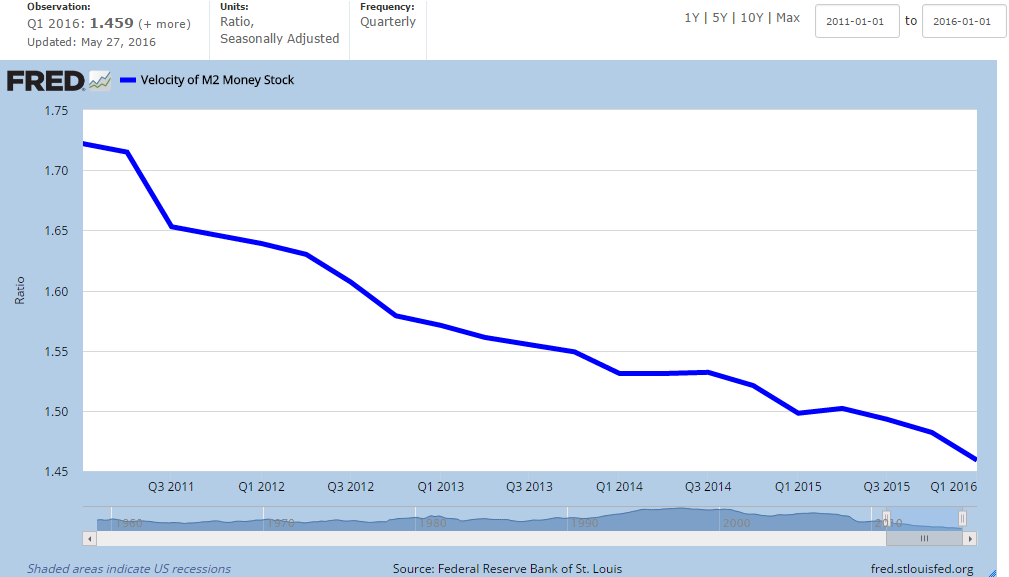

We have 5 years of declining money velocity during what has been characterized as a “recovery”.

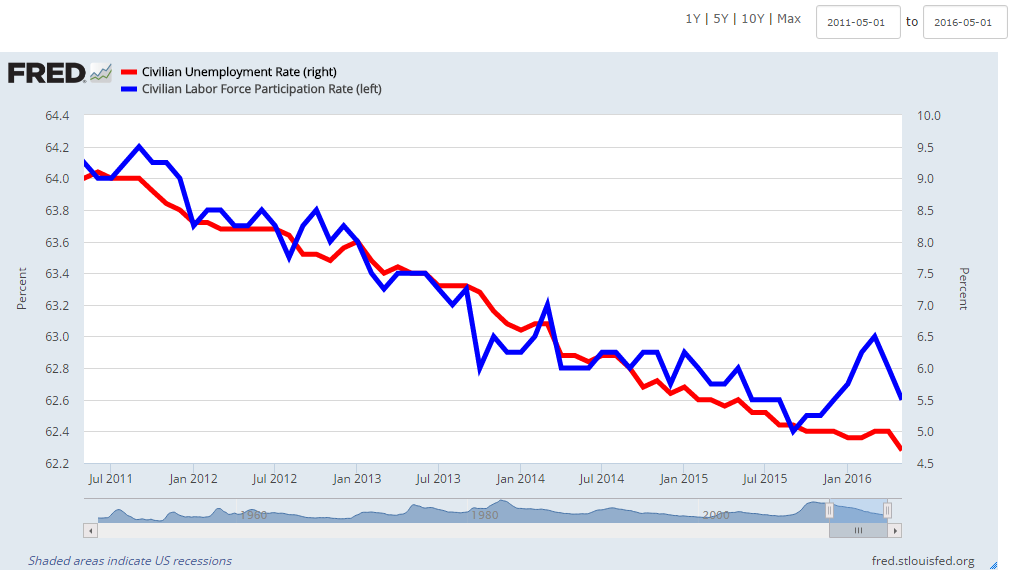

The labor force participation rate has been declining since about January of 2000. We show the last 5 years below. As to the unemployment rate, we are now well below the Fed’s measure of full employment. The labor market is now “over employed” by their own standard. Go figure data dependency on that one, my friends. They have something very wrong: it’s the central planner’s dilemma. They just don’t know the answer. Or consider the counterpoint made by a friend of the firm who is an active participant in the market, a former macro trader:

"I would argue the Fed does know the answer to labor force participation rate issue but;

- They are terrified of the structural changes (& accompanying short-term pain) it entails. This reflects the fragility of the economy and political stasis more than anything.

- They are unwilling to acknowledge that their models, policies, and transmission mechanism are broken/ineffective.

- Perhaps there's a bit of buck fever for people who have never taken real business/market risk in their lives. Markets need to clear. Bad trades need to be cut. See Japan. Absence of volatility prolongs the depression (slow, low growth) as it removes productive trauma / creative destruction from the market economy. Smoothing out the natural business cycle never works. Free market capitalism needs some volatility (read: price discovery)."

Strength of the US$

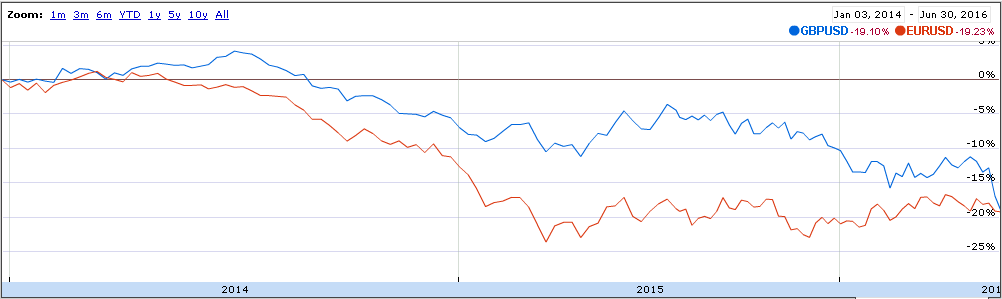

Looking back to 2014 both the GPB and the EUR have fallen about 20% relative to the US$. This puts pressure on US exporters and depresses reported earnings of non-$US revenues of US based multinationals.

ECB capital and liquidity

Our sense is that the ECB is running out of both.

“In Europe’s highly supply constrained bond market, Mario Draghi would not only have to expand his central bank's collateral pool as it runs out of eligible bonds whose yields are below the ECB's deposit floor thus making them ineligible for ECB purchases, but may have to do even more QE in a vicious loop as frontrunning the ECB leads to ever lower yields, and thus even more deflation.

Well, in March the ECB indeed announced the monetization of corporate bonds, and moments ago, in a shocking admission, Mario Draghi admitted precisely what we had warned about:

ECB SAID TO WEIGH LOOSER QE RULES AS BREXIT DEPLETES ASSET POOL

ECB OPTIONS SAID TO INCLUDE MOVING AWAY FROM QE CAPITAL KEY

ECB SAID TO BE CONCERNED ABOUT SHRINKING POOL OF ELIGIBLE DEBT

... It also means that the ECB will have to further cut its -0.4% deposit rate going even deeper into NIRP, or do away with it entirely as a gating factor for future QE purchases. The reason for this is that as of this moment, more than half the German government bonds on the European Central Bank's shopping list are ineligible for its asset-purchase programme because they yield less than the deposit rate...

We give this 4-6 months before helicopter money is unveiled.”

Source: http://www.zerohedge.com/news/2016-06-30/euro-crashes-ecb-announces-moar-qe

The Italian banks are currently problematic with huge amounts of non-performing assets and may prove a testing ground for the new "bail in" regieme, wherein creditors are transformed into equity holders and depositors can be dragged along as well, if necessary.

Other European banks are doing their own experiment, except instead of negative rates, they're trying out negative share prices. Given the complexity and inter-connectedness of the system & the atypical volatility of late, that is concerning. Sometimes that kind of movement & pain takes a while to work through the system. When large houses are down 20% in a day… and then down 20% the next day… standard normal distribution-based risk management models tend to work… poorly.

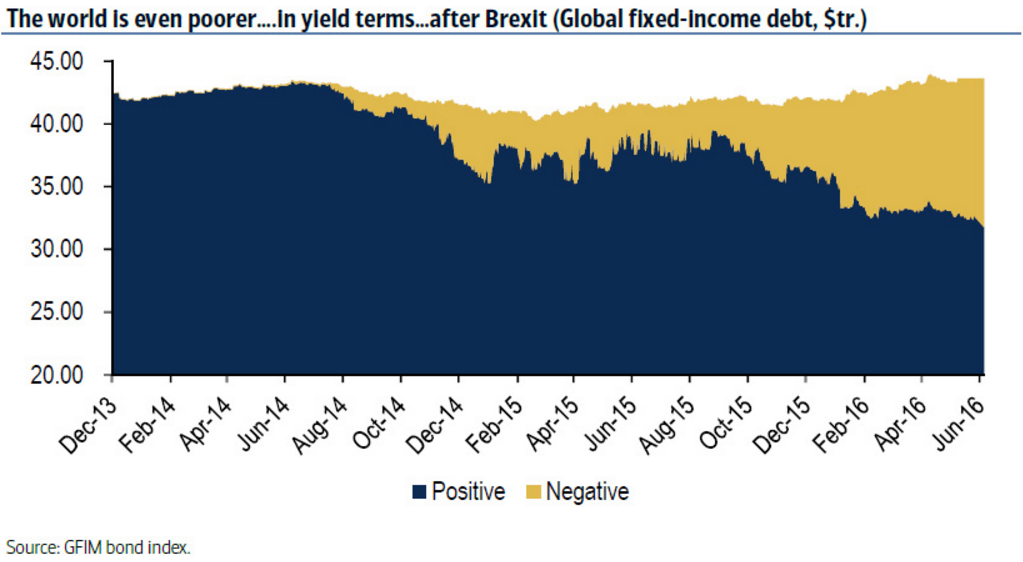

Growing spread of negative interest rates

Look at the growth. In a broad sense this is a significant portion of the global fixed income portfolio. And who owns it? Directly or indirectly pretty much everyone. Governments, central banks, private banks, insurance companies, pensions... In any event some of this is already here in the form of lower Treasury rates, and one suspects more is coming our way, either directly or indirectly. Gold's performance is notable: normalize for volatility & you avoid this entire negative rates experiment, which is unsurprising for a haven commodity.

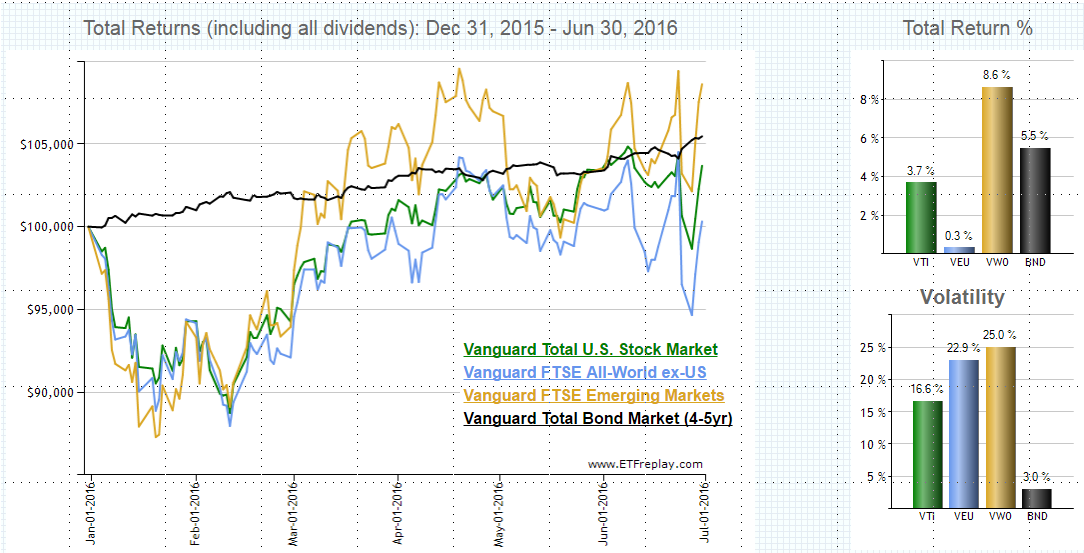

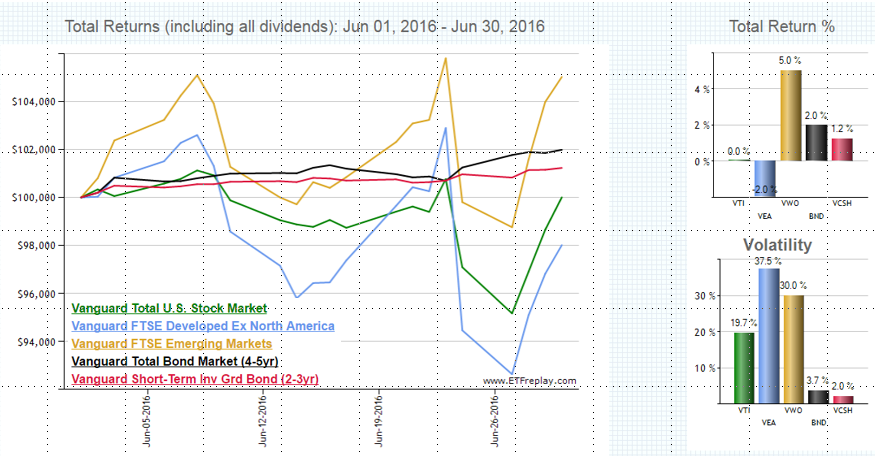

The takeaway

Below we present the ugly month of June in isolation, a look right through the heart of the Brexit beast. Here is the performance of

- US equity market,

- developed non-US equities ,

- emerging market equities,

- the US bond market and

- short term US investment grade bonds.

We stipulate that a single day drop of about 6% in non-US equities and about 3% in US equities is unnerving, but there are two object lessons for professionals and lay investors alike:

- manage risk by diversification & an appropriate asset allocation

- a panicked investor selling into a panicked market most often destroys value

And the winner of this pig pile? Emerging markets. Who knew? And that is the point: you don' t know.

...

“Look, I had a fascinating out of body experience meeting with one of the world's top central bankers in a private meeting about three years ago. And he said, "You know Kyle, quantitative easing only works when you're the only country doing it." He would never say that publicly....call it one of the four top central bankers in the world, it was a jarring experience for me, because when I look around the world today, everyone's in the same boat. So we're all trying...we're attempting through our treasury and our Fed to get the rest of the world to not devalue against us, while we quietly attempt to devalue ourselves against them, and it's all this...it is the race to the bottom.... And I believe that there is no way out.” - Kyle Bass

hb

hb

Central Banks Put Squeeze on Sovereign-Debt Market

"A buying spree by central banks is reducing the availability of government debt for other buyers and intensifying the bidding wars that break out when investors get jittery, driving prices higher and yields lower. The yield on the benchmark 10-year Treasury note hit a record low Wednesday.

“The scarcity factor is there but it really becomes palpable during periods of stress when yields immediately collapse,’’ he said. ”You may be shut out of the bond market just when you need it the most.’’

Reader Comments