On Negative Interest Rates: Whimpy Rules

An article in the Financial Times was the catalyst for this overdue posting on negative rates. Veteran bond managers Jeffery Gundlach and Bill Gross, respectively as excerpted below, sum it up nicely:

negative interest rates “are the stupidest idea I have ever experienced”, and warned that “the next major event [for markets] will be the moment when central banks in Japan and in Europe give up and cancel the experiment”.

“Global yields lowest in 500 years of recorded history…. This is a supernova that will explode one day.”

Our thoughts on the general topic:

-

Negative rates are first and foremost a taking from savers & investors for the benefit of borrowers. One might note the most levered institutions in the world are fiscally irresponsible governments, most of which could not service their debt absent artificially low rates. Negative rates are a hidden tax designed to enable and cover up excessive government spending.

-

Negative rates do not address the causes of our economic problems: defective tax, regulatory, labor, and fiscal policies which have caused massive distortion of all the markets & economic behavior they touch. And that’s a lot: the entire global economy. Negative rates will only exacerbate the problems of excess debt, malinvestment, declining labor participation and productivity. We will see even slower growth and declining productivity.

-

Negative rates add (and have already done so) massive amounts of interest rate and systemic risk to global fixed income markets. This undermines the financial stability of every owner of fixed income assets globally.

-

Negative rates in theory requires massive behavioral changes of all players in the global economy. These changes will not occur without risk & disruption. They are already being resisted & may fail or be extremely limited.

-

Negative rate theory values all consumption and at a premium to savings & investment. Such is not the case for the real economy.

And what is the scale of this phenomena? Negative yielding sovereign debt now exceeds $10 trillion dollars according to Fitch Ratings. And it spreads: according to the Financial Times more than $36 billion of corporate bonds with a short-term maturity currently trade with a sub-zero yield. This because investors seek corporate paper with positive yields which in turn drives the yields down, ultimately now to yields that are less negative than the sovereign paper.

“If you want low risk investments you have to pay for them.” - Gene Fama

...

Imagine putting in the clutch and shifting it all in reverse. In a world with positive interest rates the borrower pays the lender for use of the money. In a world with negative rates the lender pays the borrower for using the money. So we must reverse the entire global supply chain to Whimpy’s Rule: cash on Tuesday is worth more than that cash today.

And we see the institutional response already:

“Commerzbank announced that it was thinking of buying vaults to hold its excess deposits in bank notes. If rates go more deeply negative, the German bank could lower its own interest bill and offer more attractive (or less unattractive) rates to depositors.” https://next.ft.com/content/b4cbb6fc-2e56-11e6-bf8d-26294ad519fc

“According to Nikkei, and confirmed by Bloomberg, Japan's biggest bank, Bank of Tokyo-Mitsubishi UFJ, is preparing to quit its role as a primary dealer of Japanese government bonds as negative interest rates turn the instruments into larger risks, a fallout from massive monetary easing measures by the Bank of Japan. While the role of a Primary Dealer comes with solid perks such as meetings with the Finance Ministry over bond issuance and generally being privy to inside information and effectively free money under POMO, dealers also are required to bid on at least 4% of a planned JGB issuance, which as the Nikkei reports has become an increasingly heavy burden for BTMU.” http://www.zerohedge.com/news/2016-06-07/its-seismic-shift-japans-biggest-bank-quit-jgb-primary-dealer and http://asia.nikkei.com/Markets/Capital-Markets/BTMU-plans-to-quit-as-a-primary-dealer-of-Japanese-bonds

“German Munich Re which is roughly twice the size of Berkshire Hathaway Re, is boosting its gold reserves and buying gold in the face of the punishing negative interest rates from the European Central Bank, it announced...”

“Munich Re is resorting to the equivalent of stuffing notes under the mattress as the reinsurer seeks to avoid paying banks to hold its cash under the European Central Bank’s negative interest rates. The German company will store at least 10 million euros ($11 million) in two currencies so it won’t have to pay for the right to access the money at short notice, Chief Executive Officer Nikolaus von Bomhard said at a press conference in Munich on Wednesday. “We will also observe what others are doing to avoid paying negative interest rates,” he said....” http://www.bloomberg.com/news/articles/2016-03-16/munich-re-rebels-against-ecb-with-plan-to-store-cash-in-vaults

Now if our masters can not force the desired behavior on institutional investors, how will it work for everyday Americans? Imagine the scale of behavior that must change and the learning curve that touches every aspect of our economy and entire supply chain... our mentality and habit of being.

So if we analyze these scenarios, a generalized rational strategy would be to borrow as much money as you can and stuff all the cash in your very large mattress. The mattress grows in relative value every day. This is what we call an arbitrage: money in the mattress vs cash invested. It will happen. The big guys are already doing it. Alternatively, one could borrow a bunch of money and buy the biggest leveraged asset you can. Roll the dice big: go large or go home. You can walk away and flip the keys to the bank. We call this leveraged finance.

And one might ask, “What happened to my $5?”. Perhaps one might think of it as debt you did not borrow but have to repay.

The key points: negative rates

-

Subsidize borrowers at the expense of savers who are penalized

-

Are an attempt to induce specific behaviors over the entire system, both institutions and individuals. The goal is to force spending and investment that would not otherwise occur.

It remains a valid question to ask why we need these behaviours after so long a period of zero interest rates? What will negative rates do that zero rates did not? Why were zero interest rates not effective, and what policies brought us to this point in the first place? Will negative rates actually address the cause of the problems we face. We think not.

We have already seen the first wave of institutional responses which are not the desired behavior. Now imagine if we extend this phenomena to the entire complex of the US economy, and note the institutional responses will generally be a variation of our simple examples above. Will this be a risk free experiment? Again, we think not. Any impact on investment, job creation, and real productivity? Evidently Larry Fink of BlackRock and many others agree:

"...Mr Fink said that low rates were preventing savers from getting the returns they needed to prepare for retirement, so they were increasingly being forced to divert money from current spending into savings. There has been plenty of discussion about how the extended period of low interest rates has contributed to inflation in asset prices,” he wrote. “Not nearly enough attention has been paid to the toll these low rates — and now negative rates — are taking on the ability of investors to save and plan for the future.” https://next.ft.com/content/5965b5e6-fd01-11e5-b5f5-070dca6d0a0d

“In the long run, however, classical economics would tell us that the pricing distortions created by the current global regimes of QE will lead to a suboptimal allocation of capital and investment, which will result in lower output and lower standards of living over time. In fact, although U.S. equity prices are setting record highs, real median household incomes are 9 percent lower than 1999 highs. The report from Bank of America Merrill Lynch plainly supports the conclusion that QE and the associated currency depreciation is not leading to higher global output.

The cost of QE is greater than the income lost to savers and investors. The long-term consequence of the new monetary orthodoxy is likely to permanently impair living standards for generations to come while creating a false illusion of reviving prosperity.” http://guggenheimpartners.com/perspectives/media/the-monetary-illusion

We reserve a special place for Swiss Re who have been on the vanguard of sounding the warning on malinvestment, the impact on the real economy, and systemic risk. This from their seminal analysis and commentary, Financial repression: The unintended consequences :

"US savers alone have lost a whopping USD 470 billion in interest rate income, net of lower debt costs. This is just one upshot of central banks' unconventional monetary policies initially enacted to manage the crisis....

“Capital markets' ability to function well also comes under threat. Artificially low yields crowd long-term investors out of the market, preventing them from pumping savings into the real economy to stimulate growth. This reduces the diversification of funding sources to the economy, representing a risk for financial stability at large."

And this:

“Long-term investors, like re/insurance companies and pension funds, are also faced with an "opaque tax" on their investment income – as seen in the decline in running yields over recent years. Re/insurers' current high allocation to fixed income assets translates into roughly USD 20-40 billion in additional income that could have been generated over the 2008-2013 period for both US and European insurers. This also results in lower risk capital available to be put to work in the real economy.”

http://www.swissre.com/rethinking/financial_stability/turn_off_the_money_tap.html#inline

...

An implicit goal of negative rates is to accelerate spending, any kind of spending, to stimulate economic activity. We believe an erroneous assumption behind that thinking is that spending of any kind is an inherent good regardless of opportunity cost or outcome. Accelerated consumption is all that counts for old style Keynesians. And here is the problem: it’s like a distressed LBO (leveraged buyout) going on a spending binge it can’t afford and funding it with a zero coupon bond. It can live for a bit more, but the debt comes due. In the case of negative rates, the adverse outcome arrives when massive value is destroyed as artificial rates normalize.

"All debt must be repaid, if not by the borrower then by the lender. " Frédéric Bastiat

The Keynesian focus on consumption of kind at any cost is simply wrong. Consider:

“by simple analogy, if you borrow money and buy a bottle, well, let's make it a case, of Château Ausone St. Emilion 1998, and throw a kicking party, the next day all you have is a headache and the debt to pay back. You may have joie de vivre, but you are impoverished. On the other hand, if you borrow the same amount of money and buy productive assets, the next day and for all future you will have the economic production of those assets. You may be dour, but you are creating wealth, the extent of which is determined by the economic productivity of the asset in which you invested.

To modify this example for sovereign states, you simply need to make the dollars bigger (add zeros !?!) and the time frames longer. A simple, but essentially correct analogy.”http://www.wwbllc.com/commentary/2010/2/5/dynamite-in-the-hands-of-children.html

This is the kind of thinking that leads to bubbles, declining investment and productivity. Any consumption is inherently good and any investment becomes good as long as you borrow. Remember the billions of vacant buildings in China? Or the dot.com bubble? We are now in process of exporting duration, credit risk and systemic risk into global fixed income portfolio while depleting the interest income which they earn and re-invest. Some of this has spilled over into the equity markets as well. We note near record levels for the S&P and contrast it with the weakness of growth and GDP. Negative rates are the opioids, the enabler that allows defective policy and malinvestment to compound.

The magnitude of change associated with negative rates is too great to digest. The underpinnings of our real economy are too weak to support the implementation of a risky and unproven hypothetical concept. Fixed income investors have been abused too long are now are at the point where their portfolios are stacked with Fed induced risk and returns so low that long term investment objectives are threatened.

More pointedly, how does this impact individuals who have relatively modest financial capacity to bear prudently significant equity risk, say a 50 year old planning for retirement? Buy bonds for a negative nominal and worse real return? Extend duration? Buy junk bonds and hope for the best? Or take on larger amounts of equity risk? Sophie’s choice.

Try to run an insurance company or annuity firm at negative rates. Try to fund your retirement or your children’s education with negative rates. Try to adequately capitalize the financial sector with negative rates.

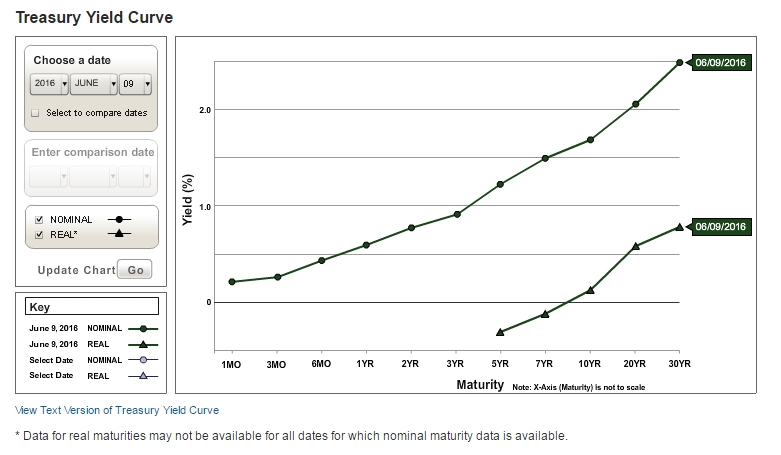

And we’re there already with real (triangles), as opposed to nominal rates (dots) :

Having exhausted my rant we now return to Mr. Fama’s comment, “if you want low risk assets you have to pay for them.” He’s right. The current prices reflect current supply and demand; however, the Fed and other central banks have had their thumbs on the scale for some time. People are buying these instruments because they are the best alternatives they see, which we take as prima facie evidence of the policy defects that brought us to this moment.

Hello, bitcoin, blockchain, and gold? Perhaps.

We recall the comment of a grizzly, seasoned crisis manager working through a distressed obligor. In the initial meeting with the bankers he opened with, “You’re not getting out. Nobody is getting out.” This, of course, turned out to be true. The only difference is that the bankers at the meeting voluntarily made the loans at inception to lend. Negative rates don’t give you a choice. Nobody is getting out of this game... unless we fix the fundamental policies.

hb

hb

Ed - we cleaned up a few typos after posting.

hb

Americans Will Spend More Than 8 Billion Hours and $409 Billion Complying With Tax Code in 2016

Perhaps a slight drag on the real economy?

hb

There’s Now $11.7 Trillion of Negative-Yielding Debt WJS 6/30/16 Wealth Adviser

Reader Comments