Observations on foreign bank liquidity

Today's WJS advises that

For the past three months, European banks have been largely unable to sell debt at affordable prices to investors, who are wary of the banks' vulnerability to risky euro-zone government bonds and other loans.

At $34 billion, the amount of senior unsecured debt issued by the Continent's financial institutions this quarter is on track to be the smallest of any quarter in more than a decade, according to data provider Dealogic. - Europe's Banks Face New Funding Squeeze

Let's see ... from more than $250 billion in QI and QII in 2009 to $34 billion.

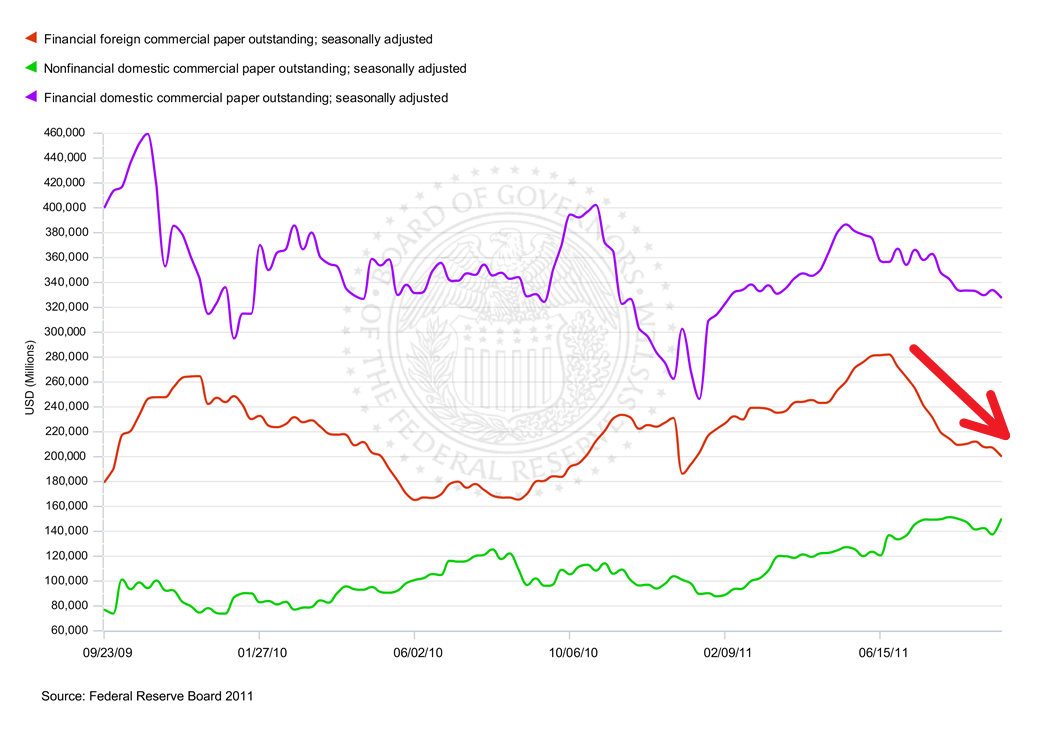

We looked at the short end of the curve and see that the foreign financials have racked up a 28% decline in outstandings since the peak in June (see the big red arrow below).

Bloomberg reports

The eight biggest U.S. money-market funds reduced their investments in French banks by 46 percent to $42 billion in the past 12 months, data compiled by Bloomberg and published Sept. 9 in the Bloomberg Risk newsletter shows.

This is particularly precarious for banks, given that liquidity pressures over year end can be stressful even in good years. Saavy liquidity managers are starting now to fund through year end, but there is, evidently, a substantially declining bid for even the shortest of foreign financial paper in our domestic markets.

Where does it go? The Euro commercial paper market is simply too small and, oops, low-to-no bid there anyway.

Below we present outstandings of various segments of the US commercial paper market:

This is the US$ funding crisis everyone's been anticipating. Last we heard France was trading around 1.96% for 5 year credit default swaps, and Italy about 5.03%, so its not clear that sovereign support for the banks will bring much to the party. The Germans need to play.

If there is some good news it is to be found in the blue & green: there is a growing supply and demand for non financial domestic commercial paper. It's good to see some credit creation, however modest and the financial outstandings seem, well, sideways is good enough.

hb

hb

The full text of Barroso's speech (you may disregard, as always, the stuff in French as not material):

For the short story: EU's Barroso State of the Union speech

Worth a read if only to see the similarity of Orwellian language and thinking with what is coming out of the White House, Treasury, and the Fed as well as the outcomes the United States needs to avoid.

hb

We are well informed that banks that were previously sitting on core assets are now looking to sell, hopefully near par, as a more cost efficient solution than funding the assets. Much of the decent stuff was given up as collateral for the covered bonds. Such is the way of liquidity triage. You sell what you can, the good stuff, and hold what you can't, the bad stuff. More to come.

Reader Comments