Kurtosis and systemic risk: policy makers need to get a clue

When we see phenomena we think we intuitively understand, and it's important, we try to kick the tires a bit. Intuition is good, confirmation by fact is better. Here we take the S&P 500 for a broad proxy of the US equity market and further take VFINX, Vanguard's 500 Index Fund, as our guinea pig. We downloaded 10 years of daily data and found some of the pictures of interest, some entertaining, one vitally important. Here we go:

Here is the time series of daily price data from Jan. 3 to Sept 27, 2011 downloaded from Vanguard. You know its ugly, but take a look anyway.

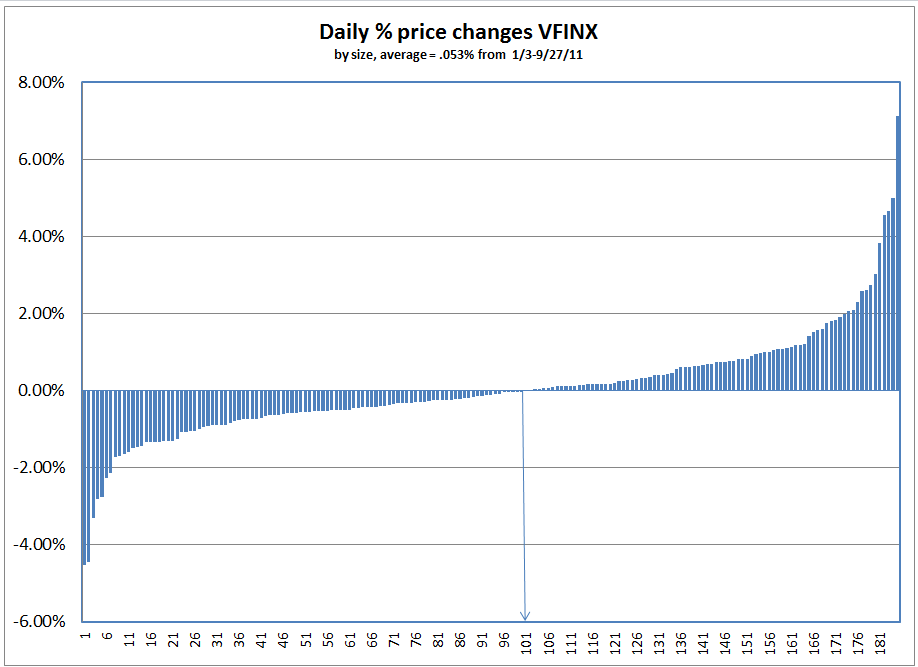

Here is the same data sorted by % size of daily gain or loss. Less ugly, but only due to style of presentation. If we hadn't put the drop down line in, it might have passed for semi normal. But it seems a little longer on the left side, yes? Of the 185 data points, 100 are negative.

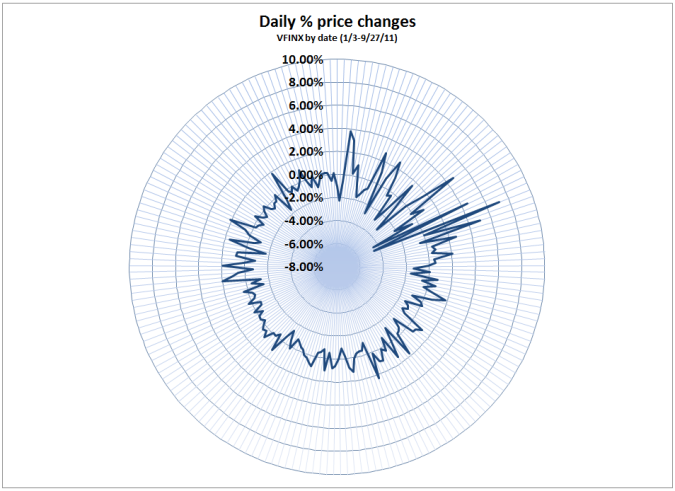

Same data displayed differently, or as a matter of conceptual art perhaps a "splatter chart" of someone's viceral reaction hitting the floor.

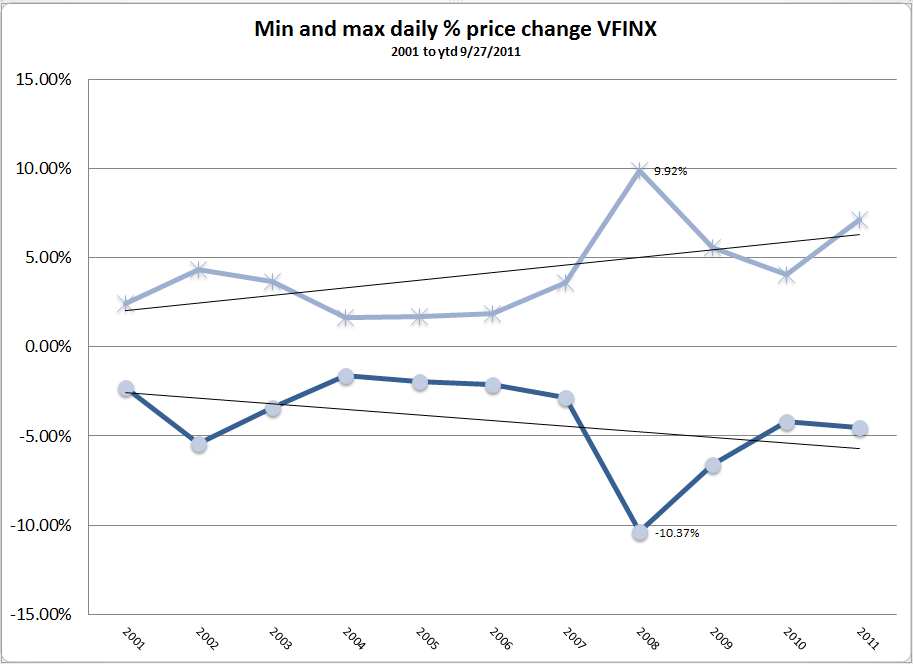

So how does this volatility stack up to a decade of price behavior? Below we chart the minimum and maximum one day % changes of the past decade (specifically from 9/21/2001 to 9/27/2011). Well, so far it seems there are only three worse years:

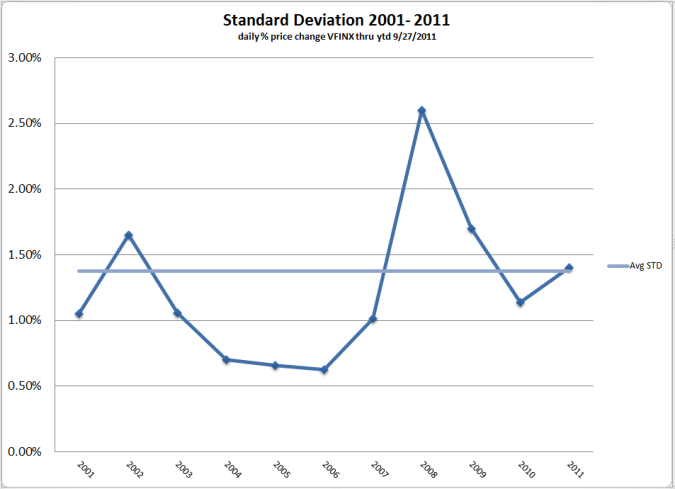

Interestingly, so far this year's standard deviation in and of itself is about average, but the dispersion seems to be increasing.

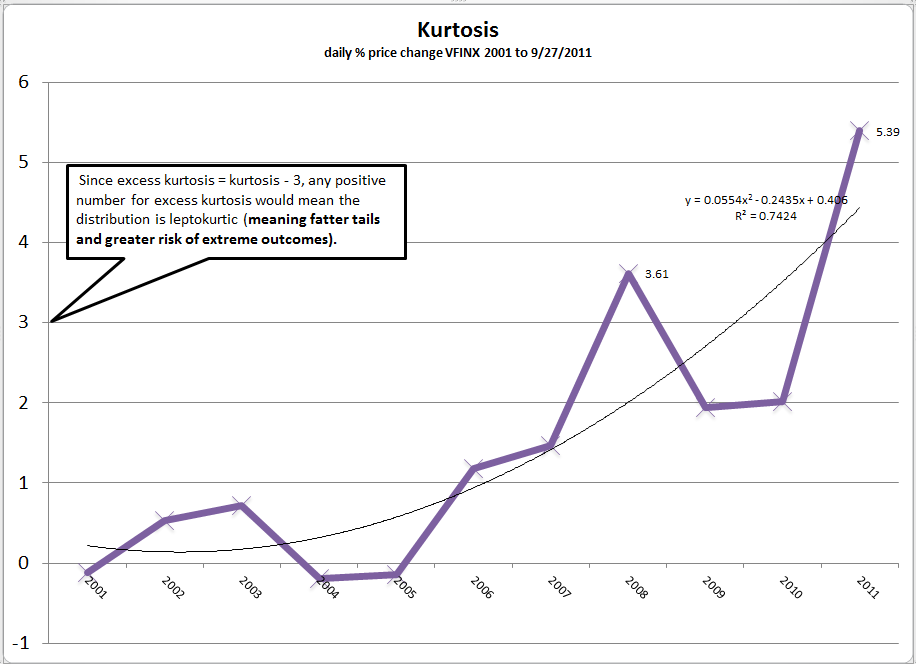

We took at look at the kurtosis over the last decade. You can see the definition in the picture (bolding courtesy of editor). The trend since mid to late 2007 is not encouraging. Others have found similar results, that is increasing excess kurtosis, in the yields of 90 day T-bills. This is systemic risk.

This bears particular import for the operation of global capital markets, and in particular for alternative assets as a class. Most of the literature we've seen indicates that adding alternative assets to portfolios of traditional asset classes can increase kurtosis of the overall portfolio (think pensions & endowments) if unartfully done. We also suspect that the notion of kurtosis induced by alternative assets isn't even examined in by most small institutional & retail investors. And certainly most alternative assets are soldpresented on the basis of mean variance risk/return space which is the quintessential apples to oranges.

Policy implications

At some point the Fed, regulators, and policy makers have to get a clue. They are manufacturing systemic risk and mere repackaging doesn't help. Granted some of this is spillover form Europe, but at the end of the day in the financial sector we still have large scale asymmetry in the treatment of the too big to fail financial sector, that in the form of socialized risk and privatized return. We are still left with increasing aggregates of black box counter-party risk.

We have utter chaos in the regulation of the non-financial sector, and we have a chaotic tax code that incents the mis-allocation of productive capital. And they continue taking economic water out of one side of the bucket to put in the other side without regard to leakage or fundamental damage to the bucket....We note that free trade bills have languished without action for the last 3 1/2 years; the Senate undertakes consideration of Currency Exchange Rate Oversight Reform Act, our very own modern version of Smoot Hawley; an energy policy designed to throttle exploration & production; and a Rube Goldberg tax code.

But the good news is that the market and the United States has the ability to suffer through the current toxcity of policy and leadership. No doubt the outcome of the election will impact valuations. Intrade now prices the probability of BHO's re-election at 47%. Even with a sensible regime change, we're in for a long slog, but we're is not ready to piss on the fire and call in the dogs1.

In the context of a seven to ten year time frame equities are not unattractive at these levels, but the meaning of the kurtosis graph is that you better buckle up. The investment premise is simple: you'd better not be investing for near term value. Getting from here to there will be the trick, and adaquate liquidity will be important. If we get some sensible policies in place and some new leadership, then the values offered today may very well look compelling 7-10 years forward. But as our President is known to say, "let me be very clear": it's going to be a bumpy ride from now to then.

____________________________________

1 Colliquial expression of cultures in the Appalachian & southwestern regions of the United States.

hb

hb

Reader Comments