Volatility: the inverse bubble

We were dismayed to see today’s WSJ article Fed Officials Growing Wary of Market Complacency only because we were working on the final draft of this posting yesterday. No matter. We recommend the better and earlier article of May 20th, Tranquil markets are enjoying too much of a good thing by Ms. Trett of the FT about the continuing decline of volatility in nearly every market. It is worrisome, and we’re not sure anyone understands why it is happening. Nor is it limited to equity markets: oil, fixed income, currencies... pick a card.

Volatility in a normal market is generally thought to be an indicator of risk. If volatility is high, things bounce around a lot, and that’s risky in the traditional sense. However, we have previously argued that the absence of volatility can also be an indicator of risk, a different and more toxic form, one perhaps induced by fear or lack of information, either with the consequence of behavior evidencing no or limited activity, a hegemony, if you will, such that all the risk books are tucked away, all the positions minimized... all wait & watch.

It’s always fun to look at asymptotic curves, so here’s one for you (and Ms. Yellen).

VXX is an exchange traded note that offers exposure to a daily rolling long position in the first and second month VIX futures contracts and reflects the implied volatility of the S&P 500® at various points along the volatility forward curve (see the 3 links detail). What if you were the unlucky fellow who bought VXX in October of 2011 for about $843? It’s now trading at ~$34. Or the lucky fellow who sold this bad boy all the way down... no matter.

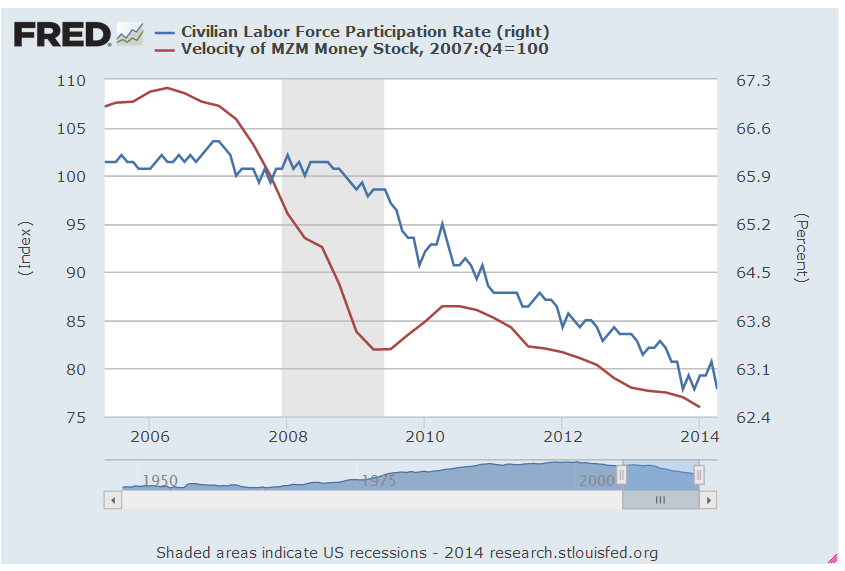

The bigger question is does this look normal? And no, it does not. And what might cause this phenomenon, this disequilibrium? Hold that thought.

Call us crazy, but we see some similarity here, if only in the category of big things going down ( this may be a bridge too far, but here goes).

These are inherently important structural things, and they all look like they are begging for a reset.

Back to volatility: by it’s essence will not go away. It may wait. Squeeze the balloon, and it will expand into another area... or pop.

If one traces the economic pressures from the market failure of 2008; to the subsequent credit problems on balance sheets of the TBTF financial institutions; to the Fed’s current balance sheet, nearly insolvent and inadequately capitalized as it may be; to the balance sheet of the US Treasury which hides unfunded off balance sheet liabilities; to the artifice of low rates; to the inflation of global asset values; to the artifice of faux capital of european banks; to ... well, where we are now... low risk? Low fear? Really?

No one would casually characterize the global geopolitical environment as low risk, nor would anyone credibly claim any clarity as to the outcomes of major domestic policies regarding tax, energy, and regulatory matters. No one would characterize the domestic political environment or leadership as predictable, so what drives the anti-bubble of volatility?

We suspect the lack of volatility is a signal event that the Fed has pushed the limits of current policy too far. We hypothesize that the Fed has operated with the consequence of impairing broad market function by depriving market participants of informational signals that they would normally receive. It’s kind of simple. How do you order your book if you are informationally deprived? Or build a factory? How do you assess value of any asset when the foundational input is a manipulated price of a treasury bond? We call to mind the old adage, “Don’t fight the Fed.”

Perhaps the Fed has beaten all into submission, at least for now?

We have previously noted on this blog some of the unintentional consequences of Fed, fiscal, and regulatory policy previously including the

-

continuing manufacture & increasing concentration of systemic risk (TBTF moral hazard)

-

a refusal to deal with the excess leverage and unfunded liabilities at sovereign, state, municipal and financial institutions

-

the mal-investment induced by prolonged negative real rates,

-

and the distortion of capital markets themselves, including acute distortion of the repo markets or occasional pricing mayhem in the bond markets

We see distortions merely transplanted and compounding, not problems resolved or cured. They have simply squeezed the balloon. We think the current low level of volatility is another unintended consequence of current policy, one driven by a false presumption of sustainable control, a presumption that is not without risk.

A massive fire in Yellowstone Park in 1988 opened the eyes of foresters to the fact that a century of wildfire-suppression, and with it competition- and turnover-suppression, had only delayed, concentrated, and by far worsened the destruction — not prevented it. This isn’t just about dead-wood accumulation creating a fragile tinderbox network. The real issue is how our tinkering artificially short-circuits the fundamental capacity of the system to allocate its limited resources, correct its errors, and find its own balance through the internal communication of information that no forestry manager could ever possibly possess. (The more this is mocked by technocratic naïfs like Geithner, the more valid it is.) But that capacity is still there, and homeostasis ultimately wins through a raging inferno. This is a cautionary tale for our economy.

Inequality, Free Markets and Crashes , a discussion with Nassim Taleb and Mark Spitznagel (which we recommend reading in whole).

hb

hb

Reader Comments