Review & outlook Q3 2014: how long will this last?

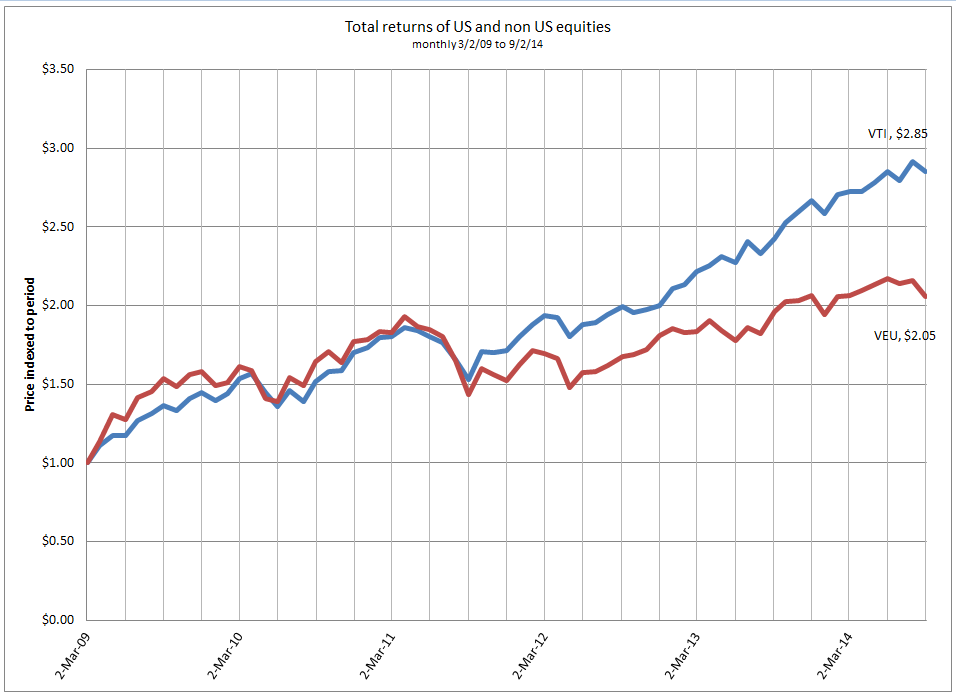

Since the market low of 2009 to date we have seen an incredible run of domestic and foreign equities. We’re in the 6th year of a ~300% cumulative bull run with domestic equities and ~200% in non-US equities. It one of the longest, if not the longest, sustained bull runs in the equity market.

Below we present total return graphs1 of Vanguard Total Market Index ETF (VTI) which represents about 95% of the tradable US market and Vanguard FTSE All-World ex-US ETF (VEU) represents an almost equally broad footprint of all non-US equities, including developed and emerging markets. It’s been quite a ride, but how long will it last?

US & foreign equities since March 2009

Our outlook

There is nothing but the election, a possible correction in the equity markets, and Ebola from now to Nov. 7th. And we all hate political commercials.

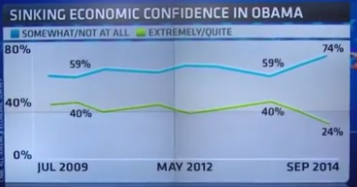

We have no particularly confident view of the markets, the economy, the domestic political landscape or geopolitical stability. We do believe our political leaders have lost credibility. They have been ineffective & disingenuous, and the word is spreading. Our country is losing confidence which wears on the economy and national morale. For example, some 74% of respondents in today’s CNBC’s poll are only somewhat confident or not confident at all in Obama’s economic policies:

Source: http://www.cnbc.com/id/102063107

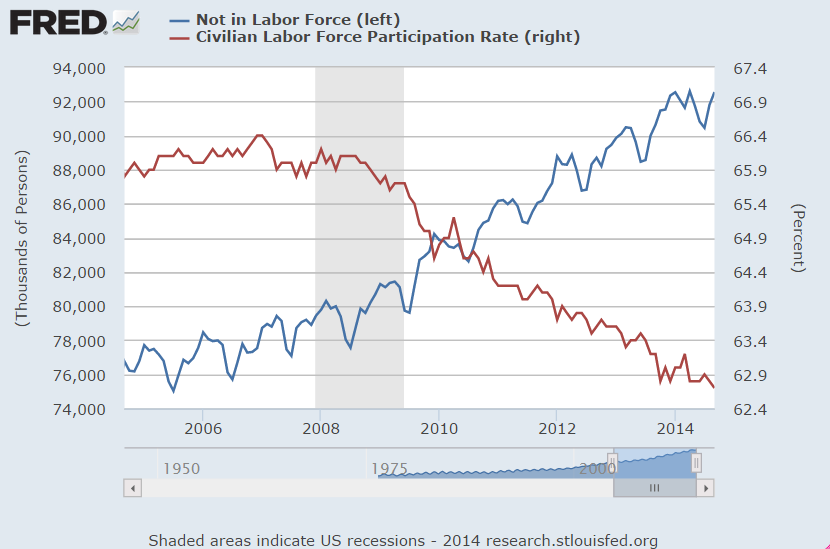

The list of global ailments is well known: Russian troops actively engaged in the Ukraine, instability of gas supplies to Europe, ISIS, and Iran going nuclear just for starters. The list of the usual domestic suspects remains the same, static for some time & without resolution: excess debt, unfunded liabilities, declining median real family incomes, systemic risk, burdensome regulations, perverse incentives, et voila, record low of labor participation rates.

We expect increasing volatility across fixed income, currencies and equities as consensus of all varieties frays. We do anticipate a correction in equities, and think, if not overdone, it would be healthy for the markets and the economy. The economy is not at an inflection point, but rather people are wondering about one.

Economic growth:

We continue to watch the labor markets, and our sense is there is slow & steady improvement although it's hard to see in the graph. The labor market and capital budgets may prove to be a fragile state of affairs if growth in Europe & Asia slows. Domestic demand will suffer.

We watch the top line of sales growth of the Fortune 1000, and it is not all that robust. FactSet reports estimates 3.6% for Q3 2014. We stipulate that corporate America does have momentum, good systems, and healthy balance sheets, and we anticipate continued slow & low grinding positive growth.

Negative short nominal rates: The Financial Times of September 25 advises that “Investors are pushing rates on Treasury Bills into negative territory because of a scarcity of safe assets as funding pressures intensify with the end of the financial quarter....Treasury bills that expire on October 2 were quoted in a price range of -0.015 and -0.02 per cent yesterday with bills expiring on November 6 quoted from 0 to -0.005 percent.”

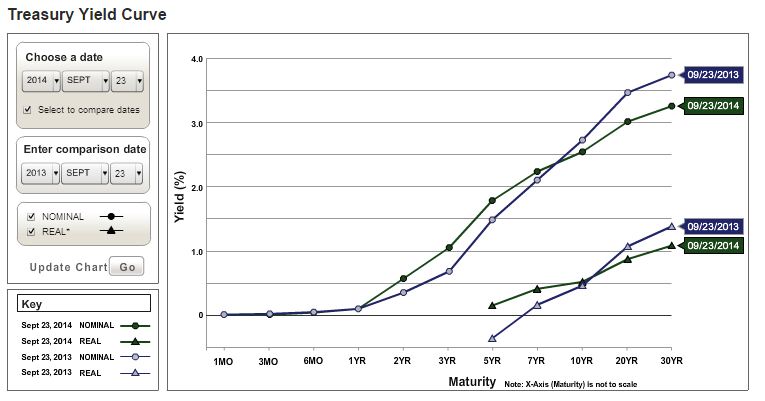

Negative real rates persist in the short end: Below is the US Treasury yield curve in real terms (as of 9/25). Real rates are negative out to 5 years.

Source: http://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=realyield

The current yield curve and that of a year ago show a slight rising of 2-7 year rates, but surprisingly a significant decrease in 10 years and out. This also seems to caution against assumptions of high economic growth, if not a warning or whiff of deflation. The astute reader will note that the Treasury seems to publish two different numbers for the real rate. Take a look at the 5 year real rates in the graph below and the text above. No doubt timing differences, but close enough for government work, we guess. The Treasury website won’t show the negative real rates under 5 years on the graph. Savers & short bond investors know why.

No consensus on the Fed: The split between the hawks & doves is getting worse. We’re generally not a fan of Blinder but he’s got the schism right. See Behind the Fed's Dovish Turn on Rates. We are confident that Yellen will continue a low rate scenario for some time, particularly if there is any adverse/weak economic data. We are equally confident that the printing presses are at the ready should deflation appear.

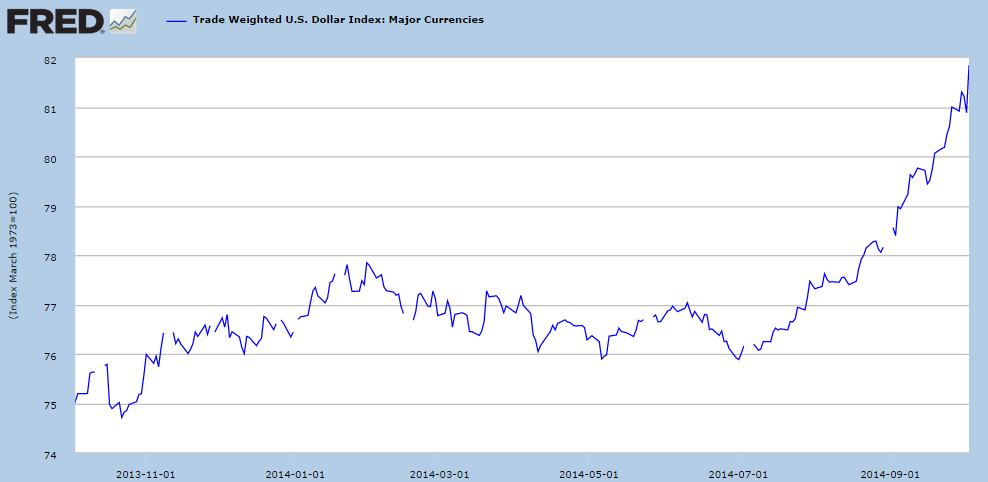

The US dollar: will continue to benefit from a flight to quality and depressed global interest rates. It’s the best looking pig in the poke. Check out the WSJ and note that virtually all foreign government bonds yield less than US bonds except Greece, Portugal, Italy, Aussies and Kiwi's. So, if you’re a Russian gangster, a very nervous & wealthy Hong Kong investor, or a global macro manager, where do you want to be? The strength of the US dollar will also support Yellen’s preference for low interest rates... imagine that.

Implications for portfolio strategy: so what do we do?

Let’s revisit the graph of the equity markets at the top of this posting. Go back and look at it. An aging bull market and concerns of a correction would suggest a tilt to underweight equities a bit. This begs the question of market timing. We don’t think you dump and run. You get smarter and tighten the risk & liquidity bolts. Our clients have been selling into this bull market for many years just by virtue of rebalancing. Still, looking at the chart one just can’t help wondering...

“if only I had bought a 3x leveraged S&P ETF in March 2009...”

Well, you didn’t. Here’s why: you were terrified in March 2009 because the market had just collapsed, had just given you about a 48% haircut in about 6 months. It was a dark time, and people were scared. Institutional investors didn’t fare much better. They generally didn’t sell before the crash or buy at the bottom. Why not? Why didn’t we all sell or buy at the right time? Because you can’t.

Timing the market is not a very constructive effort. Why do we say this? Take a look at the performance of tactical asset allocation funds over time2. That’s what they do: market timing. But it doesn’t appear that they do it as well as you might think, or in the case of their investors, hope.

- "We find no evidence that manager selection, market timing, and tactical asset allocation generate alpha."Source: Do (Some) University Endowments Earn Alpha? updated May 2013, by Brad M. Barber, Gallagher Professor of Finance, Graduate School of Management UC Davis, and Guojun Wang, Ph.D. Student, Department of Economics, UC Davis

- “Conclusion: In extending our study of tactical mutual funds through Dec. 31, 2011, we found that tactical funds generally struggled to deliver competitive risk-adjusted returns when compared with a traditional balanced fund. With a few exceptions, they gained less, were more volatile, or were subject to just as much downside risk as a 60%/40% mix of U.S. stocks and bonds. These findings largely reaffirm our earlier study of tactical funds. In addition, we also found, in a simulation of various hypothetical portfolios over the 10-year period ended Dec. 31, 2011, that the average tactical fund would have delivered little incremental diversification.” Source: In Practice: Tactical Funds Miss Their Chance, Jeffrey Ptak, 2/2/2012, Morningstar Advisor

- "The obstacles to successfully pursuing real-time defensive portfolio reallocations include the low predictive power of even the best signals of bear markets and recessions, the strategies' potentially high transaction and tax costs, the inconsistent performance of asset classes over time, the long delay between when recessions begin and when they are confirmed in economic statistics … and the often-narrow trading window in which one has to act. Finally, defensive (read reactive) investing comes with a considerable and underappreciated cost—not being strategically invested in the equity market when the bad times end." Source: Recessions and balanced portfolio returns by Vanguard.

If the tactical asset allocators can’t do it, why do you think you can?

The importance of asset allocation as a risk management tool

Long term investing is about time in the market, not timing of the market, with an asset allocation that carries an appropriate level of expected risk, one that the investor can prudently tolerate, in exchange for an expected level of return over an intermediate to long time frame. And the essential element is to make sure you know the risk and can carry it. Ok, so what is the risk?

Equity risk: how big, how long, how ugly?

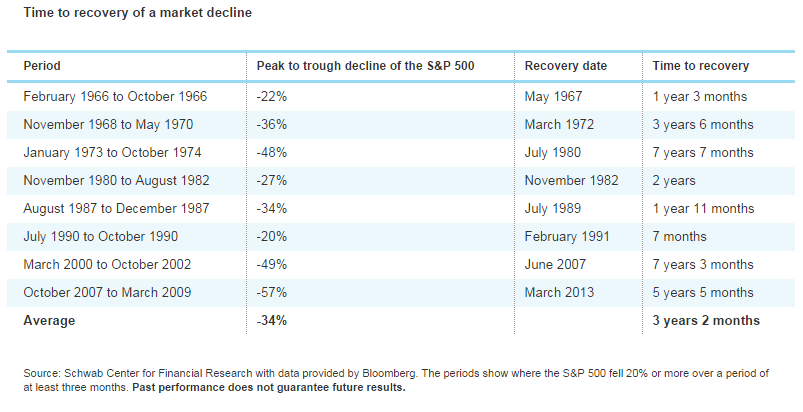

Over the last 50 years the average bear market for the S&P 500 lasted a little more than one year, and time to recover was a little more than 3 years.

Source: http://www.schwab.com/public/schwab/nn/articles/Retirement-Income-Planning-Whats-Your-Risk-Capacity?cmp=em-QYD

One might be tempted in the 6th year of a old bull market to dump & run, and short term investors may well do that. Long term investors, however, have additional risks to consider:

“Well ... if we sell all the equity, we have no more equity risk, but we also have no more equity returns. All we have left is fixed income and essentially a huge exposure to inflation risk. And do we re-enter the equity market? When? We have a lot of evidence that suggests we’re simply not good at timing the market, in fact, we’re pretty bad at it.”

Inflation risk: bigger, longer & uglier?

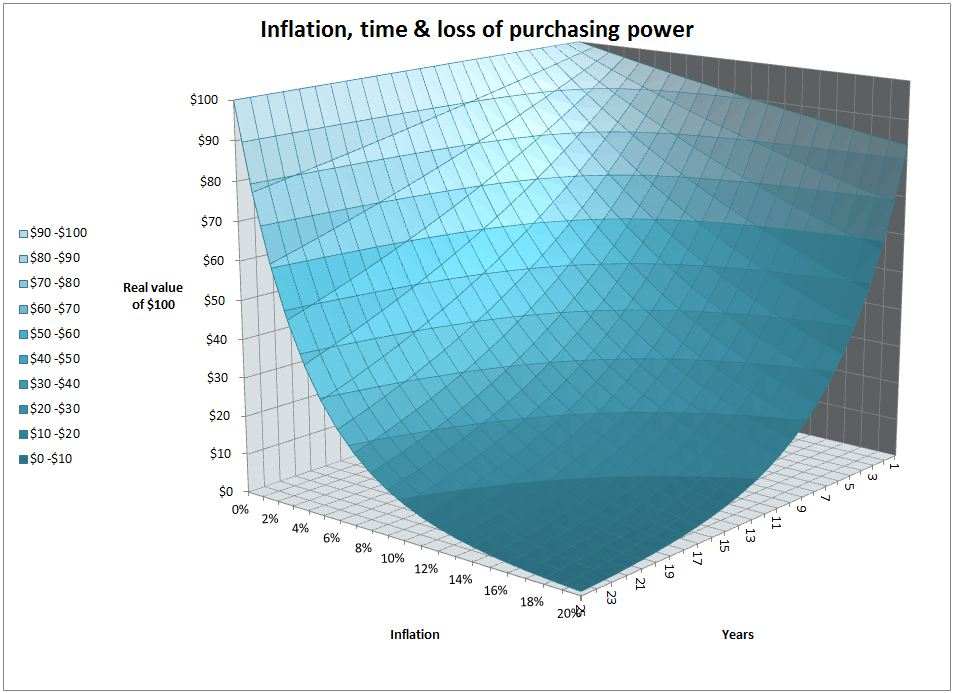

In our view inflation is the biggest single risk facing investors3. It erodes, with permanent loss, the real purchasing power of capital. There is no 3+ year average time to recovery.

Look at our favorite graph below which shows that even very modest levels of inflation pose a significant loss of purchasing power over long periods of time. Here’s an important hint: if you’re getting into the shaded or darker blue areas, you’re looking at losses of more than 70% of economic value, permanent deadweight loss. It never comes back.

Source: http://www.wwbllc.com/commentary/2013/9/20/the-taper-of-q3-actual-results-may-vary.html

It just so happens that high real returns are the only protection against inflation... and that generally means equities. So our counsel is to keep your eye on the appropriate timeframe of your investment horizon.

For many of our clients it is a generational matter and the question is how to sustain yourself, how to build liquidity and a risk profile, such that you have the ability to ride out the bumps and retain the ability to compound real returns over long periods of time.

The necessary ingredients for a successful portfolio strategy are:

- an appropriate asset allocation that presents

- a level of risk you can carry

- executed with low costs and

- adequate liquidity that accords you the confidence & staying power you’ll need

Your plan should include adequate liquidity to get you from here to there, to allow you the time required to capture & compound real returns. If you don’t have it, your plan needs a touch up.

Fear is the mind killer and destroys wealth. Get ready to buy back to target.

...

Footnotes:

- The growth of value including reinvestment of dividends for the indicated time period, rebased to starting date. Historical data from Yahoo Finance, graph by WWB.

- “Tactical asset allocation” is a strategy that essentially relies on timing the markets & placing bets on different asset classes. So, for example, they try to buy stocks before they go up and sell them before they go down. Or do the same with bonds or whatever asset class they can take a shot at. So, a tactical asset allocator might shift you from 90% equity/10% bonds to the inverse if he thought the equity markets were going to tank.

- We’re ignoring taxes for the moment. Never ignore taxes...

hb

hb

Reader Comments