Friday

Jul082011

“greek finance building on fire. euro to new highs. twilight zone”

Thus commented a young trader on 6/29/11. We took it for our cover quote on our Q2 2011 market commentary of 6/30/11 some of which is excerpted below.

- The quote reflects the ‘fog of war’ in the global markets. Anticipate more.

- We see a challenge to Western democratic capitalism as sovereign credits have melded with financials. The deterioration of both is a function of sustained failures of ethical leadership, agency risk, and governance. Economic mis-management of such scale poses a particular challenge to the market oriented, republican democracy of the United States.

- Our circles believe that we have moved well past a crisis of confidence.

- Europe will continue to muddle through the Greek restructuring with Portugal and Spain to follow, and we anticipate the standard of living in Euroland will slowly and ever so surely decline over time.

- We leave to you to assess the probable outcomes of Congress meddling with the primal forces of the tax code & budget priorities. The menu as we see it comprises

- a default, either technical or substantive;

- a quick & bad fix; or

- a good & substantive fix.

- We haven’t even mentioned the elections…except to say we encourage all investors to get directly involved.

- We don’t know whether the last minute 400 or so point run in the Dow was driven by hedge funds trying to drive up Q2 performance (as was suggested by a manager of a $1 bn fund) or whether the market is starting to price in some probability of favorable changes in policy & governance. Champagne uncorking on rumors of Geithner’s resignation?

- We confess we don’t have a cohesive view of where the markets are going and will not apologize for it. We sense that uncertainty is great, but stand contradicted by relatively low volatility. VIX has taken the role of a contra indicator?

- We remain biased against US$ duration as a function of risk & magic by ‘the Bernanke’ . We still see some value in credit spreads as a defensive fixed income play (“well, its not equity…”). The yield on short term investment grade corporate debt (VCSH, ~2.8 duration) exceeded the 5 yr. Treasury of June 27 by ~ .40%.

- The yield on the Dow (DIA) is about equal to the 7 yr. Treasury and ~12x forecast earnings, not unattractive.

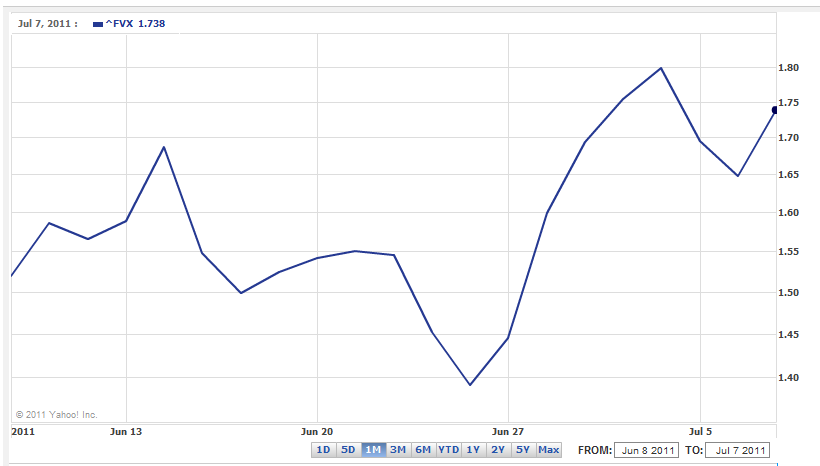

In the main, however, major risk now takes the form of a known unknown (we know we don’t know it): the outcome of political process of regulatory, tax & budget reform. We must note the extraordinary volatility of the 5 year Treasury yield and offer our condolences to anyone who had the temerity to be long on June 26 or 27.

Lastly, just to keep you sleeping well, was there a leak in the informational pipeline in advance of the downgrade of Portugal that moved the market? Welcome to the Twilight Zone.

hb

hb

Reader Comments