Maybe the Fed doesn't have Yahoo or Google finance?

Here we see the price behavior over the last 3 months of certain proxies of asset classes of interest:

- energy (via the proxies XOM and OIL),

- precious metals (GLD and SLV);

- commodities (GSG),

- 30 yr US Treasury yield (^TYN); and

- US $/EURO rate (EURUSD).

Those of us who are color blind may have difficulty discerning the finer points, but in some sense the colors don't matter. The blink test is sufficient. Annualize the gains, and you get some non-trivial numbers.

The only things going down are the US $ and the credibility of the Fed. Oh, we forgot, short US interest rates too ... with thanks to Johannes Gensfleisch zur Laden zum Gutenberg who invented the essence but not the jargon of 'quantitative easing'.

We have, once again, Nassim Taleb tearing a very public and much deserved strip off Bernanke (its worth the full viewing), and Bill Gross in Run Turkey Run uses the failing credibilty of the Fed to induce fear:

Check writing in the trillions is not a bondholder’s friend; it is in fact inflationary, and, if truth be told, somewhat of a Ponzi scheme.

which Gross then turns into a marketing ploy:

We hope to be your global investment authority for a new era of “SAFE spread” with lower interest rate duration and price risk, and still reasonably high potential returns. For us, and hopefully you, Turkey Day may have to be postponed indefinitely.

Oh, my. We don't necessarily disagree with his analysis, but find the style a little heavy handed... but that was before the Asian finance ministers cut loose with the 12 guage OO buck shot.

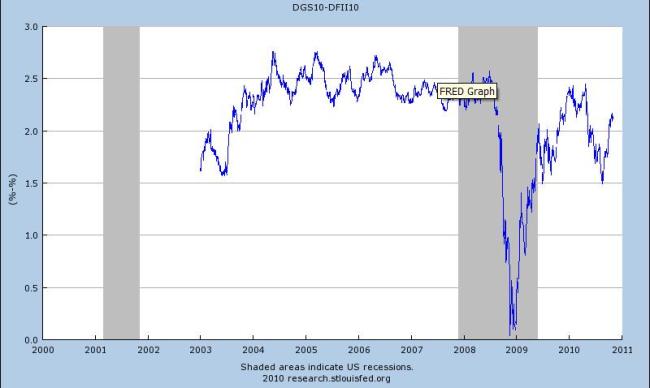

The spread between nominal bonds and TIPS (inflation indexed bonds) is a quick proxy for inflation expectations, and we note the same trend as the picture above:

10 year constant maturity treasuries less 10 year TIPS:

Of course, over the weekend, right in the middle of this drafting, all hell broke loose in a Fresh Attack on Fed Move .

The good news, though perhaps not for the Fed, is that important new independent sources of inflation data are making their way into the public arena. Wal-Mart's data would appear to be more current than the Fed's and reflective of actual sales to the consumer:

A new pricing survey of products sold at the world’s largest retailer [WMT 53.99  -0.14 (-0.26%) ] showed a 0.6 percent price increase in just the last two months, according to MKM Partners. At that rate, prices would be close to four percent higher a year from now, double the Fed’s mandate. Source: http://www.cnbc.com/id/40135092

-0.14 (-0.26%) ] showed a 0.6 percent price increase in just the last two months, according to MKM Partners. At that rate, prices would be close to four percent higher a year from now, double the Fed’s mandate. Source: http://www.cnbc.com/id/40135092

Meanwhile the Financial Times reports Google to map inflation using web data We have every expectation that whatever eventuates from this initiative will be better, faster, cheaper, more precise, and, dare we say, potentially less biased, than the Fed's. Call it a measure of just in time inflation...

We confessed our bias to short duration some time ago and suggest everyone watch the 10 year Treasury. We suspect there will be some credit turbulence in Europe. Let's just hope it stays there. Pending sensible resolution of some of the major fiscal, trade & regulatory issues, there is still a fair amount of risk that could quickly compound or boomerang. We don't believe the nominal rise in equities is a panacea, although we'll take it, and we think there is still a fair bit of political & policy risk implicit in these price levels.

If the Fed and Congress have gotten a whiff of the smelling salts, it will have been a good start. One suspects the Fed has already damaged its credibility, and if they keep pushing the Gutenberg agenda as a proxy for the failure of tax and fiscal policy, the public may very well ask the bald question: "Why do we need more monkeys throwing darts?"

hb

hb

Reader Comments